Stocks ended a volatile week on a positive note, shaking off geopolitical concerns and trade uncertainty to rally strongly into the close of February. The S&P 500 rebounded 1.6% on Friday, while the Dow Jones Industrial Average gained 601 points, and the Nasdaq surged 1.6%. This late-session surge came after a week marked by turbulence stemming from geopolitical tensions, trade policy developments, and mixed economic data.

Friday markets initially struggled amid a heated White House exchange between President Donald Trump and Ukrainian President Volodymyr Zelenskyy. Their contentious meeting raised concerns over geopolitical stability, as President Trump suggested Zelenskyy return when he is “ready for peace.” Additionally, Treasury Secretary Scott Bessent signaled that Mexico may match U.S. tariffs on China, with similar encouragement directed toward Canada. The uncertainty surrounding global trade relationships added to market jitters.

Despite these concerns, Wall Street found relief in economic data suggesting that inflation remains in check. The core personal consumption expenditures (PCE) price index, the Federal Reserve’s preferred inflation gauge, rose 0.3% in January and 2.6% annually—the smallest annual increase since early 2021. However, personal spending declined 0.5%, marking the largest monthly drop in nearly four years, raising concerns about economic momentum.

Treasuries reacted to the mixed economic picture, with the 10-year yield falling five basis points to 4.23%, contributing to a 19-basis-point decline over the week. This suggests investors are weighing slowing growth prospects alongside hopes for eventual Fed rate cuts. The Atlanta Fed’s GDPNow model revised its Q1 GDP forecast sharply downward, now projecting a 1.5% contraction versus prior estimates of 2.3% growth.

Market strategists remain divided on the path forward. UBS Global Wealth Management’s David Lefkowitz maintains a positive stance, emphasizing that the bull market remains intact but expects higher volatility in the near term. Infrastructure Capital Advisors’ Jay Hatfield pointed to the geopolitical landscape, arguing that markets may ultimately respond positively if Trump successfully brokers a peace deal. Meanwhile, Northlight Asset Management’s Chris Zaccarelli expressed caution, citing high valuations, policy uncertainty, and a market overly dismissive of recession risks.

Looking ahead, investors will be watching key economic data releases, including the February ISM Manufacturing Index and January Construction Spending, for further insights into the state of the economy. With geopolitical developments, trade negotiations, and Fed policy speculation all in play, markets remain poised for further swings in sentiment.

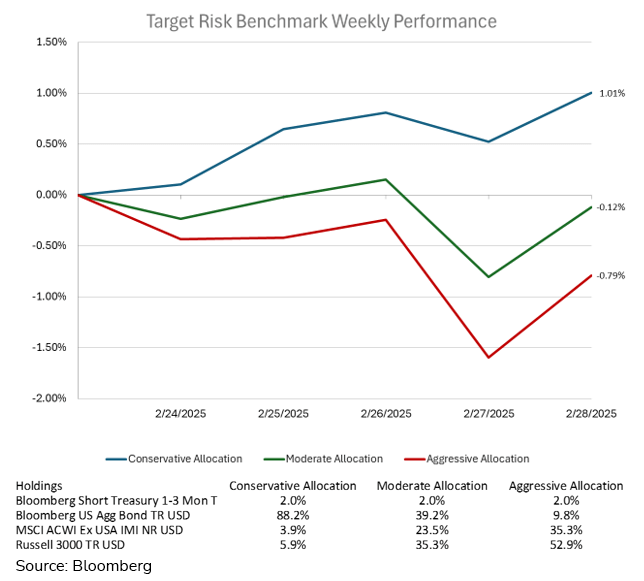

For the week, the aggressive target risk benchmark declined -0.79%, while the moderate benchmark slipped -0.12%. The conservative benchmark finished the week up 1.01% as bond yields declined.

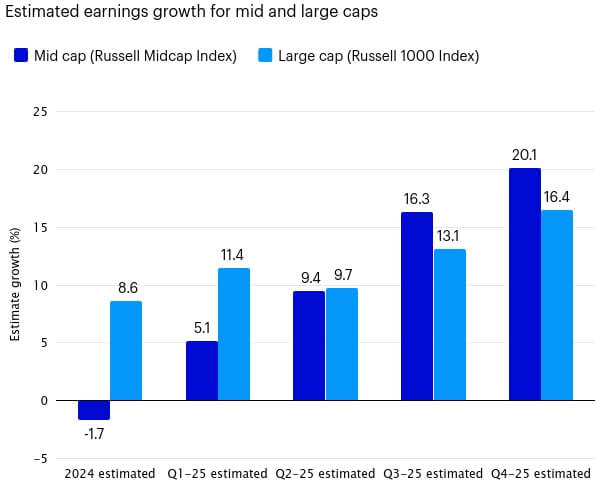

Mid-cap stocks have quietly assumed market leadership from large caps, marking a shift in equity dynamics. This rotation, already in motion, presents an increasingly attractive setup for 2025. The recent broadening of market performance suggests mid-cap stocks may be poised for sustained outperformance. Historically, mid caps have demonstrated superior long-term returns, with an 11.0% annualized gain since 1991, surpassing both small and large caps. They have outperformed large caps 56% of the time and small caps 92% of the time over rolling five-year periods. This track record underscores their potential as a compelling investment opportunity. Earnings growth projections for mid caps are also favorable, with 2025 estimates exceeding those for large caps. Additionally, mid caps trade at lower valuations, offering a more attractive risk-reward profile. While the Fed’s policy trajectory remains uncertain, its stabilization of interest rates has alleviated financing headwinds for mid caps, whereas small caps still face significant refinancing risks. Furthermore, potential government policies favoring domestic production and corporate tax reductions could disproportionately benefit mid-sized companies, given their domestic orientation. Another critical advantage of mid caps is their superior diversification. Unlike large caps, which are heavily concentrated in a few mega-cap technology stocks, mid caps span a broader array of industries, offering greater opportunities for active stock selection. The small-cap universe, meanwhile, has contracted due to a lack of new IPOs, with many top-performing small caps maturing into mid caps instead. Given the resilient economy and accommodative monetary policy, the outlook for mid-cap stocks remains optimistic.

The post-election economic landscape remains largely unchanged, with economic fundamentals appearing solid despite persistently negative public sentiment. A striking example of this disconnect is the sharp decline in consumer confidence, as evidenced by a 6.7% drop in the Conference Board's February index—the largest since 2021. Similarly, the University of Michigan’s consumer sentiment survey and various business confidence measures reflect growing pessimism. However, tangible economic indicators suggest stability. January saw strong job growth, a slight decrease in the unemployment rate, and continued low levels of unemployment claims, with the exception of Washington, D.C., where federal budget cuts have led to disruptions. A closer analysis offers insights into why confidence is faltering. Initially, post-election optimism—especially among businesses—may have inflated sentiment metrics, making the recent downturn more of a correction than an outright collapse. Additionally, partisan divisions play a significant role; while Democrats have grown markedly more pessimistic, Republicans remain optimistic, and independents show little change. More importantly, the anxiety appears to stem from future expectations rather than present conditions, with assessments of the current economy remaining stable since October. Inflation concerns are a primary driver of uncertainty. January’s consumer price inflation rate was 3%, above expectations, though the Fed’s preferred measure is trending closer to 2.5%. While Trump is not being blamed for past inflation, his proposed tariffs on imports have sparked concerns over potential price increases. However, investor and economist expectations do not align with consumer fears, suggesting a disconnect between perceived and actual inflation risks.