Financial markets experienced a turbulent week, marked by sharp fluctuations in response to economic data, tariff developments, and geopolitical shifts. The S&P 500 endured significant volatility, dropping before staging an "oversold bounce" following comments from Federal Reserve Chair Jerome Powell, who reassured markets that the economy remains stable. Meanwhile, the Nasdaq 100 briefly entered correction territory before recovering. Investor sentiment was in part shaken by trade policy uncertainty after U.S. President Donald Trump followed through on new tariffs, sending the S&P 500 below its 200-day moving average for the first time in months. Despite a late week rebound, the index posted its worst weekly performance since September. Wall Street also digested mixed labor market data, with U.S. job growth slowing to 151,000 in February and the unemployment rate ticking up to 4.1%, adding to uncertainty. Bond yields edged higher, with 10-year U.S. Treasuries rising to 4.31%, while commodities saw modest gains, with WTI crude up 1% and gold remaining stable. Bitcoin and Ether fell, reflecting risk-off sentiment.

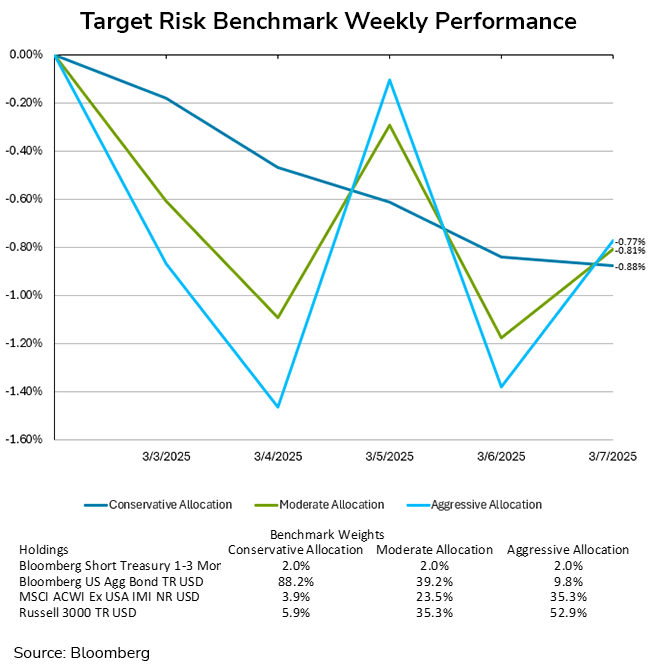

This difficult market environment resulted in losses for the week for investors of all risk tolerances. The high equity volatility saw aggressive and moderate portfolios whipsawing violently from day to day but trimming losses to end the week. Despite the recovery on Friday, the aggressive target risk benchmark ended with a loss of -0.77% for the week, while the moderate target risk benchmark ended the week down -0.81%. Bonds yields rose for the week as well, leading the conservative target risk benchmark to also end the week with a substantial loss of -0.88%.

President Trump’s tariff increases on imports from Mexico, Canada, and China risk causing stagflation—a mix of slowed economic growth and rising prices. Economists warn that these tariffs could disrupt business investments, weaken household income, and raise inflation, making a recession more likely. While some officials suggest a tariff rollback may happen, uncertainty remains. Many businesses, including Best Buy and food importers, expect to pass increased costs onto consumers. Stock markets have responded negatively, with companies like Best Buy experiencing significant share declines. The Fed faces a challenge in addressing tariffs' effects since they simultaneously drive inflation higher while potentially hurting employment. Fed officials, including John Williams and Alberto Musalem, acknowledge the risk of inflation rising above the central bank’s target, drawing comparisons to past stagflationary periods like the 1970s. Despite previous warnings of stagflation that never materialized, some economists argue that tariffs could create lasting economic challenges.

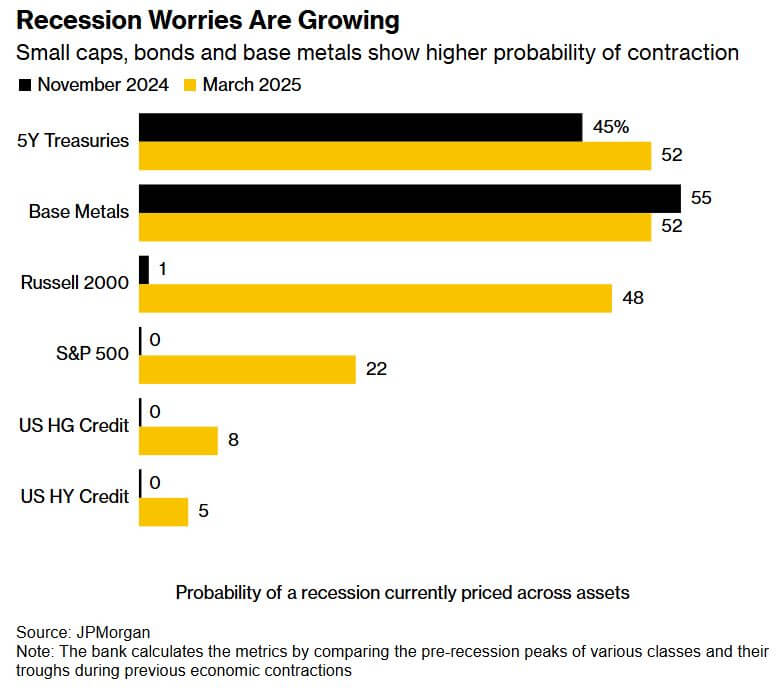

Financial markets are increasingly signaling recession risks due to tariff uncertainty and signs of economic weakness. JPMorgan Chase estimates a 31% probability of a downturn, up from 17% in November, while Goldman Sachs raises its estimate to 23% from 14%. Indicators like five-year Treasuries and base metals suggest an even higher risk of contraction. Market volatility has risen as investors react to President Trump’s tariff policies, which have dampened business and consumer confidence. Economic data shows U.S. factory activity near stagnation, declining consumer confidence, and weaker personal spending and housing reports. Despite recession concerns, some economic strengths remain, such as low unemployment and resilient income metrics. Analysts caution against overinterpreting weak survey-based data, though economic growth appears more reliant on fewer key drivers. While stagflation fears grow, the overall outlook remains uncertain.

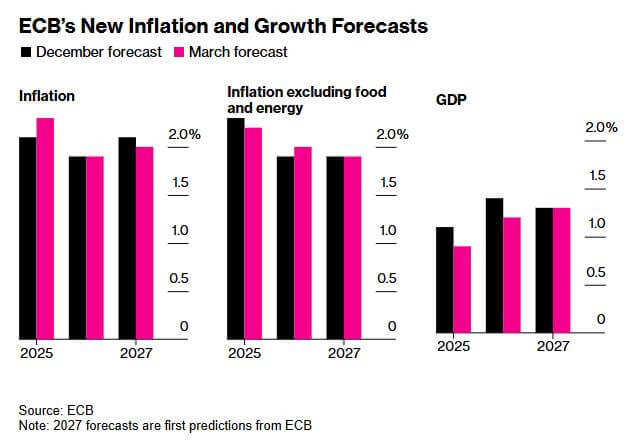

The European Central Bank (ECB) has reduced its deposit rate by 25 basis points to 2.5%, marking the sixth consecutive cut since June. However, ECB President Christine Lagarde signaled that the easing cycle may be nearing its end as inflationary pressures moderate and geopolitical uncertainties reshape economic expectations. The ECB’s new stance, described as “meaningfully less restrictive,” reflects a shift to an adaptive approach where further rate cuts or pauses will depend on evolving economic data. The ECB’s revised forecasts indicate that inflation will reach its 2% target by early 2026, later than previously anticipated, while economic growth projections for 2025 and beyond have been downgraded. Financial markets reacted immediately to the ECB’s announcement. The euro strengthened, German bond yields rose, and traders reduced expectations for further rate cuts, now pricing in only 43 basis points of additional easing for 2025.

The economic outlook remains complex. The ECB acknowledges that uncertainty could dampen investment and trade, but it also sees potential growth from rising incomes and lower borrowing costs. Additionally, Europe is preparing for a substantial fiscal expansion, with the EU aiming to mobilize approximately €800 billion for defense spending in response to changing US foreign policy. While this surge in military investment could boost economic activity, it also risks exacerbating fiscal pressures and unsettling bond markets. The euro-area economy expanded more than initially estimated in Q4 2024, with GDP rising 0.2%—double the prior estimate—driven by consumer spending and business investment. However, the pace of growth slowed significantly, reflecting uncertainty from domestic political instability in Germany and France, as well as geopolitical shifts following U.S. President Donald Trump’s re-election. Wage growth, a key inflationary driver, moderated to 4.1% year-on-year, down from 4.5%, reinforcing confidence in the disinflation process.