A rally in major tech stocks helped U.S. equities rebound after losses earlier in the week driven by weak forecasts from key companies like FedEx, Nike, and Micron. The S&P 500 recovered and turned positive for the week, with Tesla and Boeing among the top performers, with Boeing supported by a new fighter jet contract. The recovery comes amid significant market volatility, including the expiration of $4.5 trillion in derivatives. Over the past month, investor concerns over slowing growth, high tech valuations, tariffs, and geopolitical risks have erased trillions from U.S. stock values. Dip-buying strategies have struggled, and Morgan Stanley’s Michael Wilson predicts that equity prices will stay below recent highs until at least mid-year, calling this phase a "rolling recovery." Trend-following funds (CTAs) have gone net short on U.S. equities for the first time since 2023, while retail investors poured over $12 billion into the market in a single week, potentially signaling that the bottom has not yet been reached. Despite fears about tariffs and economic slowdown, some analysts say a recession is unlikely. Analysts also believe that trade risks, while still present, are less severe than earlier perceived, with expectations that actual tariffs may be lower than headline numbers suggest.

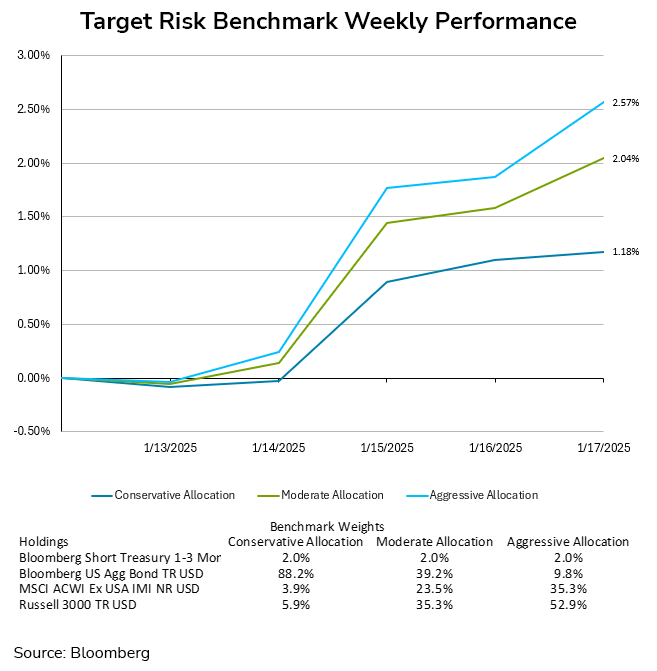

The high volatility in equities resulted in a roller coaster ride for moderate and aggressive investors for the week. The aggressive target risk benchmark finished the week with a gain of 0.32%, while the moderate target risk benchmark had a slightly higher gain of 0.37%. Conservative investors did not see the same degree of volatility, and the conservative target risk benchmark finished the week with the best result of the three indexes with a gain of 0.45%.

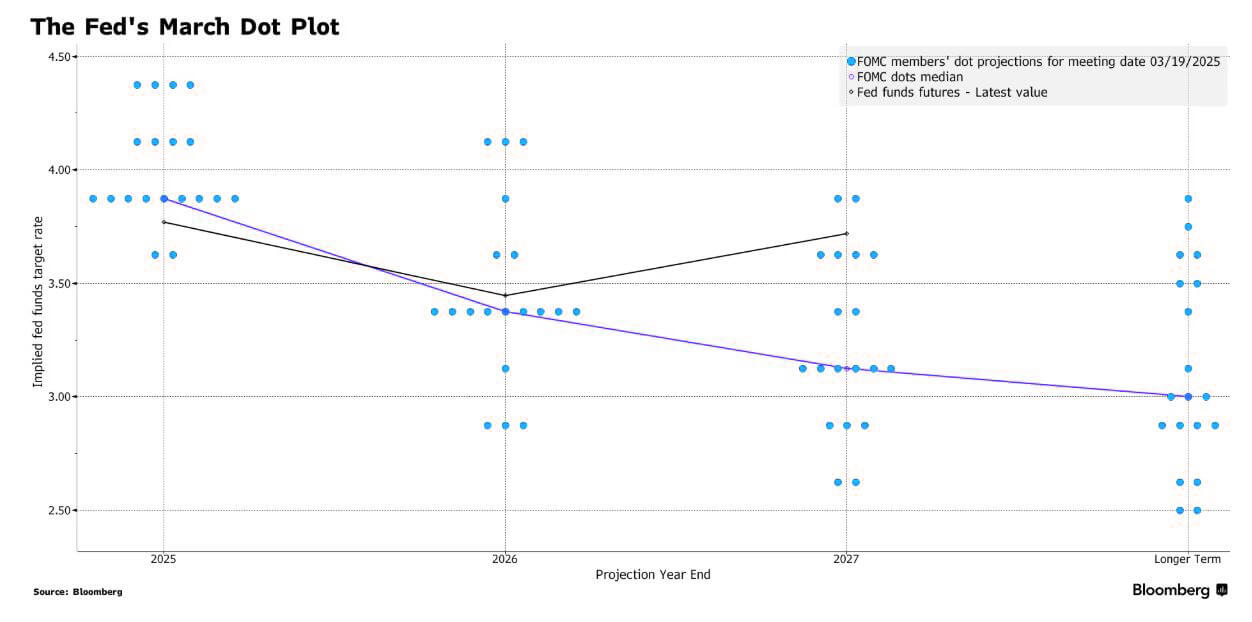

The Federal Reserve has maintained its current monetary policy stance, keeping the benchmark federal funds rate at approximately 4.3%, while adjusting its economic projections to reflect rising inflation and slower growth. Policymakers now anticipate that inflation will rise to 2.7% in 2025, a slight increase from prior estimates, due in part to newly imposed tariffs. Concurrently, GDP growth expectations for 2025 have been revised downward from 2.1% to 1.7%, reflecting increased economic uncertainty. A narrowing majority of Fed officials now support at least two rate cuts this year, compared to the broader consensus seen in December. The Fed also acknowledged heightened uncertainty surrounding economic conditions, removing language from its policy statement that previously suggested balanced risks to inflation and employment. Additionally, the central bank has decided to slow the reduction of its $6.8 trillion asset portfolio to mitigate potential financial market instability. Beginning in April, the Fed will allow $5 billion in Treasury securities to mature without reinvestment each month, a significant reduction from the prior $25 billion. Economic indicators remain mixed. While consumer spending has slowed, the labor market has remained resilient, with the unemployment rate standing at 4.1% as of February. However, businesses have expressed concerns about policy-driven uncertainty, particularly regarding growth prospects and investment decisions. Tariff policies have further complicated inflation forecasts, as their effects on pricing remain uncertain. Fed officials remain wary of inflationary expectations becoming entrenched, as businesses and consumers may preemptively adjust pricing and wage-setting behaviors in response to anticipated cost increases.

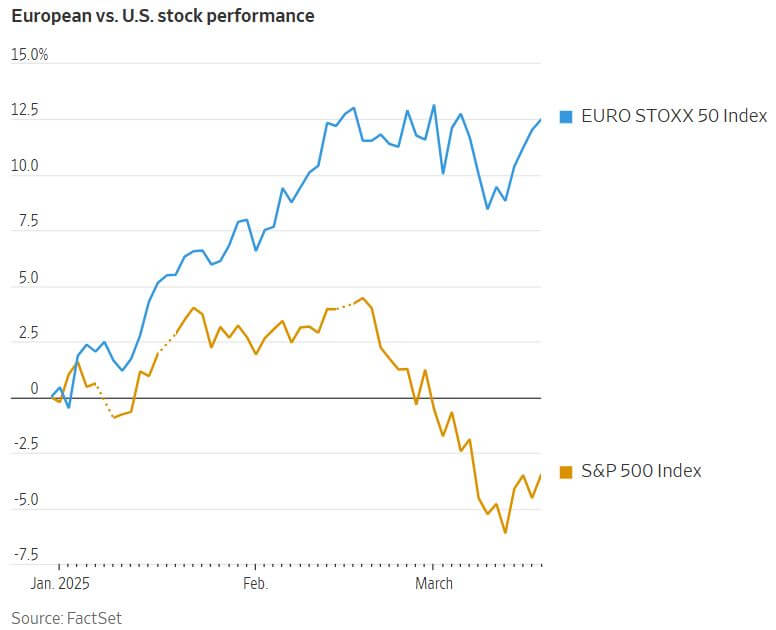

At the World Economic Forum in Davos, Europe was seen as the economic underdog compared to a bullish U.S. under President Trump. But since then, market sentiment has flipped. European stocks have risen, while the U.S. market corrected, and growth expectations in the U.S. have dropped due to weak data and the impact of Trump’s trade policies. In Europe, economic fundamentals haven’t significantly improved, but several positive shifts are occurring. Trump’s foreign policy—especially his stance on NATO, Russia, and trade—has pushed European leaders to prioritize economic and defense independence. This shift is not just financial but also psychological, marking a break from Europe’s post-crisis austerity mindset. The EU is proposing a €150 billion defense fund, while the U.K. and France are also rolling out pro-growth reforms, including infrastructure expansion and nuclear energy investments. Germany has approved a historic €1 trillion ($1.08 trillion) spending package aimed at revitalizing its economy and reducing reliance on U.S. military support. The package includes major investments in both defense and civilian infrastructure, enabled by a constitutional amendment that exempts this spending from strict fiscal rules. It marks a dramatic policy shift for Berlin, long known for its fiscal conservatism and underinvestment in defense. It includes funding for military hardware, cybersecurity, intelligence, and civil protection, as well as €500 billion earmarked for transport, digital infrastructure, and climate-related projects over 12 years. Experts caution, however, that the investment alone won’t deliver long-term benefits unless accompanied by structural reforms in taxation, labor markets, and bureaucracy. The plan could boost GDP by 2.1% by 2027, Allianz estimates, though it may raise public debt to 68% of GDP—still modest by international standards. Success hinges on swift and effective implementation, with economists stressing that without unpopular reforms, the plan’s full potential won’t be realized.