Wall Street experienced heightened volatility as stocks rebounded sharply, capping their strongest weekly rally since 2023. This came amid easing pressure from longer-term Treasury yields and the dollar, after days of market turmoil that raised concerns about waning foreign appetite for U.S. assets. While the S&P 500 surged 2% following reassurances from a Federal Reserve official about potential market support, analysts cautioned against interpreting the gains as a definitive market bottom. Uncertainty remains the defining feature of the current financial landscape, driven by escalating U.S.–China trade tensions, ambiguous fiscal policy, and shifting investor sentiment. Despite a 90-day tariff pause from President Trump, investors are retreating from U.S. assets in favor of more stable international markets. A recent MLIV Pulse survey revealed that 50% of investors intend to reduce exposure to U.S. markets, signaling skepticism over the administration’s trade maneuvers. Market strategists and economists continue to warn of elevated recession risks, underpinned by signs of weakening consumer sentiment and surging inflation expectations. Market breadth and momentum indicators suggest possible capitulation, but experts like Michael Hartnett of Bank of America argue that U.S. exceptionalism is eroding, recommending caution until there’s a clear de-escalation in trade tensions and the Fed intervenes more decisively.

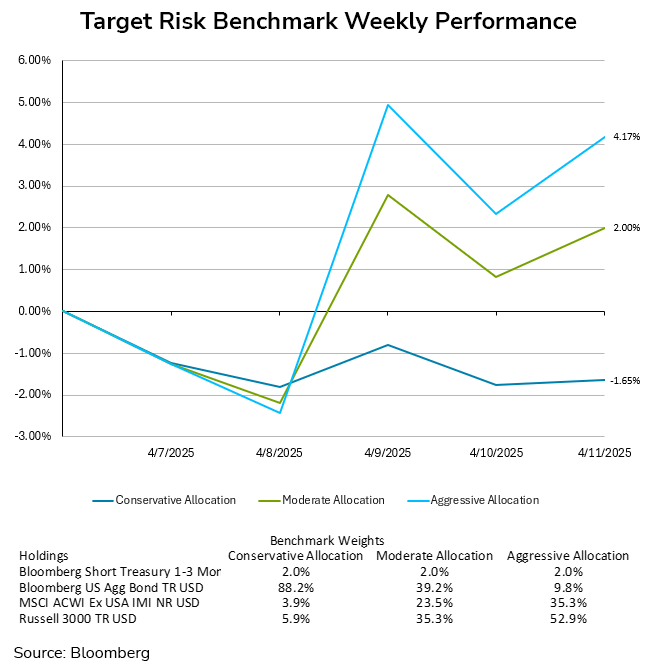

The rebound in stocks benefited aggressive investors after the prior week’s losses. The aggressive target risk benchmark recovered by 4.17% for the week, while the moderate target risk benchmark enjoyed a bounce of 2%. Counterintuitively, the conservative target risk benchmark fared the worst, falling by -1.65% for the due to the selling pressure seen in fixed income.

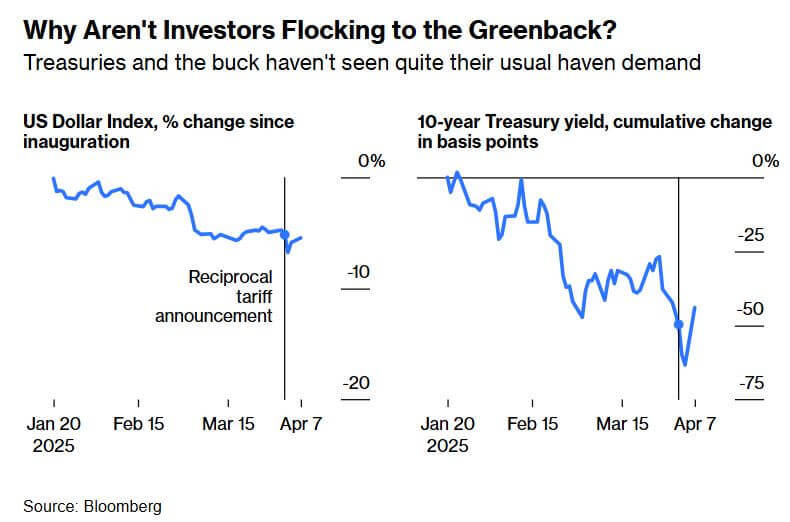

Recent market volatility underscores a shifting global perception of U.S. financial leadership amid escalating trade tensions. As President Trump intensified tariffs on multiple countries—including China, Canada, and Mexico—the S&P 500 declined by 19% at one point from its February 19, 2025 peak. More striking, however, has been the atypical market response: the U.S. dollar fell 4.5%, and bond yields rose—despite growing recession fears—suggesting investors no longer view U.S. assets as the default safe haven. Traditionally, market turmoil prompts a flight to safety, boosting demand for the dollar and Treasuries. Yet concerns over persistent inflation, policy unpredictability, and geopolitical isolation have eroded confidence in the U.S. as a stable anchor. The dollar’s role as a global reserve currency—central to international transactions and foreign-exchange reserves—remains critical, but recent behavior indicates a subtle re-evaluation by global investors. President Trump’s temporary tariff pause reversed market declines but did not fully restore confidence. Economists suggest that technical factors, such as hedge fund liquidations, may have contributed to rising yields, but more fundamentally, the U.S. is perceived as less predictable and more antagonistic under current trade policies. This shift is evident in the outperformance of gold over inflation-protected Treasuries—signaling that investors may now prefer gold as a safe-haven asset. With foreign holders owning roughly a third of all U.S. Treasury debt and budget deficits exceeding $2 trillion annually, reduced global appetite for U.S. assets could raise borrowing costs and expose the U.S. to new economic vulnerabilities, despite its historical reserve currency insulation.

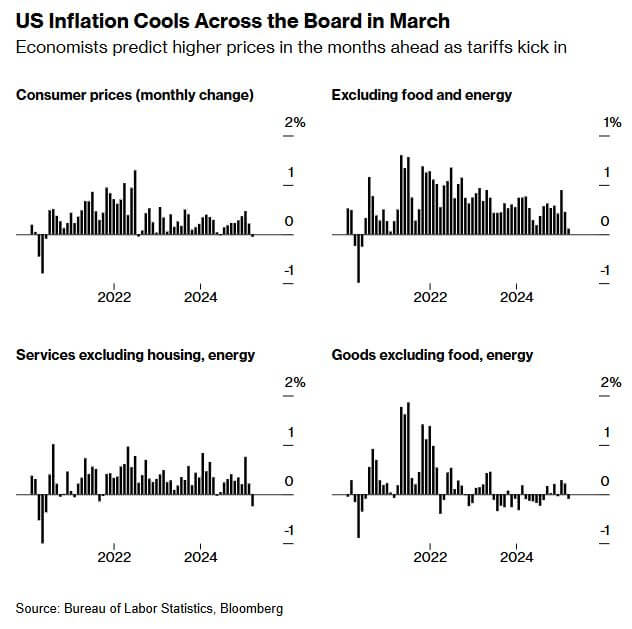

In March, U.S. consumer prices declined 0.1% month-over-month—the first decrease in nearly five years—driven primarily by a sharp 6.3% drop in gasoline prices and a 5.3% decline in airline fares. Year-over-year inflation cooled to 2.4%, below economists’ expectations of 2.6%, while core inflation, excluding food and energy, rose 2.8%, the smallest annual increase since March 2021. Although the data appeared encouraging for consumers and the Fed, economists cautioned that the relief may be short-lived due to the impact of newly announced trade tariffs. President Trump’s April 2 announcement of sweeping tariffs—later partially paused—has created uncertainty in financial markets and prompted economists to revise inflation forecasts upward. While some tariffs on goods from Mexico, Canada, and China were enacted in March, the full effects of the broader tariff policy will not be reflected until future CPI reports. The Fed, which meets again in early May, acknowledged in its latest meeting minutes the possibility of inflation proving more persistent due to external pressures such as tariffs. Despite solid labor market data, with 228,000 jobs added in March, consumer and business sentiment has weakened. The National Federation of Independent Business reported its sharpest drop in optimism since mid-2022, and corporate leaders, including those at Delta and Walmart, cited economic uncertainty and declining consumer confidence as risks to growth. Overall, while March’s inflation data offers a momentary reprieve, looming tariff-related cost pressures are expected to challenge the Fed’s efforts to maintain price stability and economic growth in the coming months.