U.S. equity markets retreated to end the week, erasing earlier gains after Federal Reserve Chair Jerome Powell signaled a cautious stance on monetary policy, disappointing investors hoping for intervention amid ongoing trade tensions. Powell’s remarks emphasized a "wait-and-see" approach to trade-driven inflation, which unsettled markets that had anticipated more aggressive support from the central bank. Investor sentiment was further strained by geopolitical uncertainty and a mixed bag of economic data. Jobless claims hit a two-month low, suggesting labor market stability, but a sharp drop in the Philadelphia Fed Index signaled manufacturing weakness. Meanwhile, trade negotiations remain volatile, with country-specific deals — notably with Japan and the EU — being closely watched, especially after broad U.S. tariffs were introduced and then partially suspended. Bond yields fell for the week, while the dollar extended its third week of losses, reflecting broader concerns about policy consistency. Energy stocks outperformed, driven by a 5% surge in WTI crude amid geopolitical tensions with Iran. In contrast, health insurers lagged after UnitedHealth cut its earnings forecast. Alphabet shares fell on antitrust concerns, while Eli Lilly surged on positive clinical trial results. Amid these developments, market participants are increasingly focused on the implications of political interference in central banking and the evolving global trade landscape. Analysts warn that undermining the Fed’s independence could significantly disrupt financial stability, particularly if trade policies continue to drive unpredictable market responses.

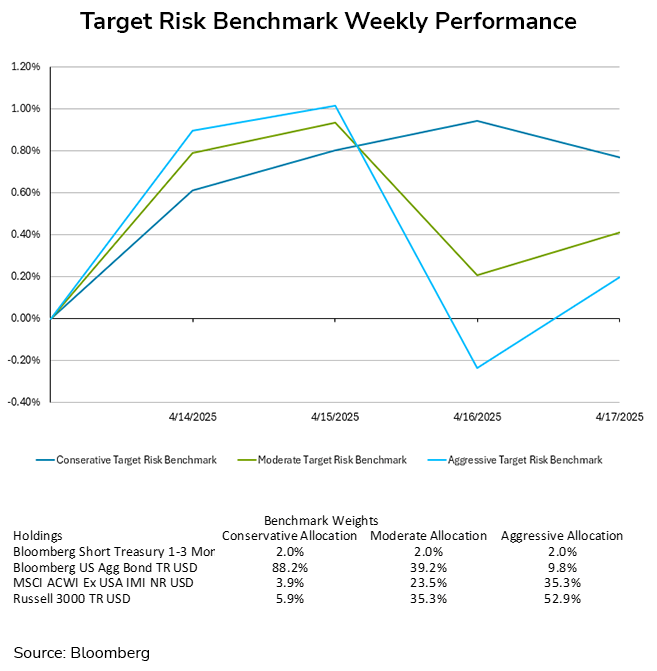

Last week saw conservative investors fare better than moderate and aggressive investors. The bond market calmed with yields declining for most of the week, resulting in the conservative target risk benchmark finishing the week with a gain of 0.77%. The moderate target risk benchmark finished with a small gain of 0.41% thanks to a rally in international stocks, while the aggressive target risk benchmark finished in last with a small gain of 0.2% for the week.

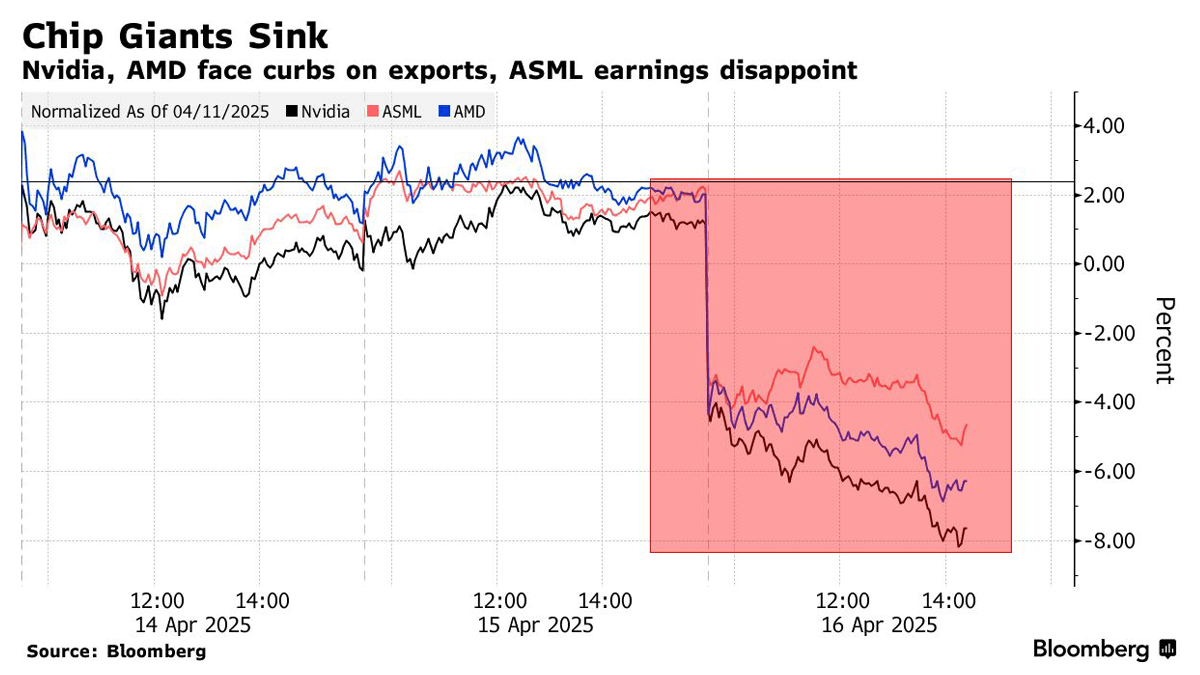

Technology stocks declined sharply Wednesday as new U.S. export restrictions on advanced semiconductor sales to China rattled markets. Nvidia and AMD led losses, with Nvidia projecting a $5.5 billion charge due to the licensing requirement on its H20 AI chips, and AMD anticipating up to $800 million in related costs. ASML Holding also fell after missing order forecasts, while the broader Philadelphia Semiconductor Index dropped 3.72%. The U.S. mandate, which now requires a license to sell chips such as Nvidia’s H20 and AMD’s MI308 to China and select countries, represents a significant escalation in U.S.-China tech tensions. While the H20 chip was engineered to comply with prior export restrictions and features significantly reduced performance—about 75% below Nvidia’s top-tier H100—it remained in high demand, particularly in China. The new policy renders even this compliance-driven approach ineffective, underscoring the growing unpredictability of regulatory barriers. Although the H20 chip contributes a modest portion of Nvidia’s expected $182 billion in data-center revenue for the fiscal year, the sudden loss of access to the Chinese market undermines Nvidia’s ability to meet aggressive growth expectations. Investors had anticipated a 56% year-over-year revenue surge, now thrown into question. The restrictions came just one day after Nvidia announced a $500 billion investment to build AI supercomputers in the U.S.—a move widely viewed as an effort to align with the Trump administration’s push for domestic manufacturing. Despite such efforts, CEO Jensen Huang’s high-profile engagement with President Trump appears insufficient to shield the company from the broader trade policy fallout. Ultimately, Nvidia's situation illustrates the vulnerability of even industry leaders to geopolitical risk. The company’s dominance in AI is now challenged not by competitors, but by policy decisions that reshape global technology supply chains.

With the risks and opportunities facing the sector, investors may wish to consider diversified large cap growth managers with quality tilts rather than strategies that are restricted to only the technology sector. Diversified growth managers offered on the Freedom Advisors platform include Zacks Focus Growth and Neuberger Berman Large Cap Disciplined Growth.

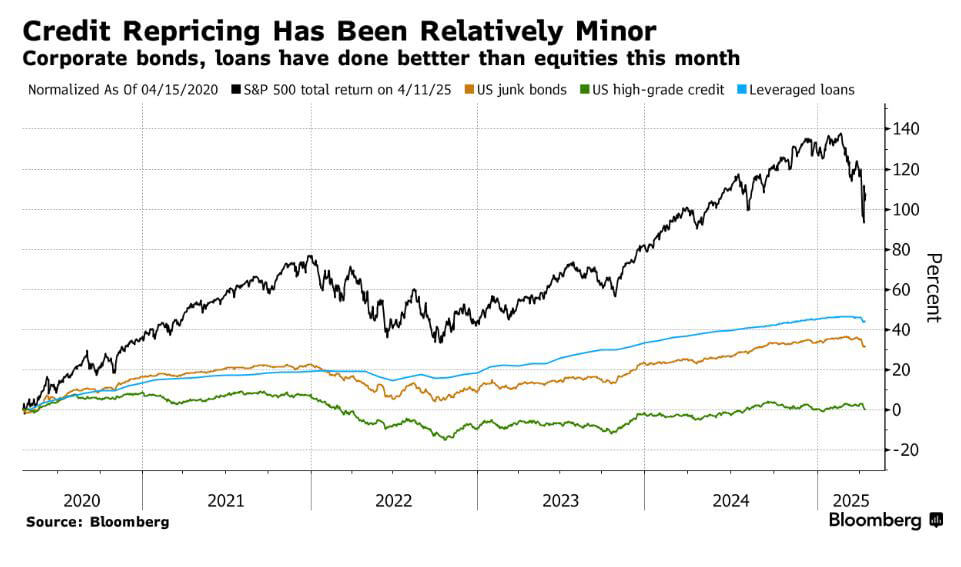

The recent escalation in trade tensions has rattled credit markets, ending a prolonged period of calm. Risk repricing has been swift but orderly, with corporate debt spreads widening significantly—though not yet reaching crisis levels. Credit default swap (CDS) spreads have jumped the most since 2020, and high-yield spreads, particularly in BB and B-rated debt, have risen to levels last seen in late 2023. The riskiest bonds (CCCs) reflect elevated default concerns, though still below recession-era peaks. Investors are recalibrating expectations, anticipating potential policy reversals amid shifting global trade dynamics. However, current spread levels suggest the market is pricing in a relatively mild economic impact from the trade war—possibly underestimating the severity of risks. U.S. protectionism poses a structural threat to credit markets. Export-reliant companies and those with global supply chains face significant headwinds, and import-dependent firms could see margins squeezed. Persistent policy uncertainty is weighing on capital investment, hiring, and M&A activity, raising the risk of a downturn without triggering panic. Despite the volatility, credit markets remain functional. Primary issuance has continued, with high-grade issuers leading and riskier borrowers following during calmer intervals. While new-issue concessions have widened, investor appetite for high yields remains strong, supported by reduced supply and persistent demand. Private lenders also provide a backstop, offering capital at a premium for execution certainty. Still, credit markets may be underpricing the potential fallout. A prolonged tariff regime could fundamentally impair corporate balance sheets, especially among leveraged borrowers in retail, auto, and energy. Those facing near-term refinancing at high rates are particularly vulnerable. For now, optimism prevails, but growing macroeconomic risks could swiftly reverse sentiment.

For investors who wish to participate in the upside offered by credit relative to Treasuries but are concerned by the risks posed by any potential widening of credit spreads, a tactical approach to fixed income exposure may be an option. Tactical fixed income strategies offered by Freedom Advisors include Kensington Managed Income and Ocean Park Strategic Income.