Global markets treaded cautiously as the U.S. and China prepared for trade negotiations, with equities and bonds showing minimal movement. Investors appeared skeptical that the talks would yield a comprehensive breakthrough, especially after a sharp $6 trillion recovery in the S&P 500. Trading volumes were subdued, reflecting broader hesitation. President Trump’s proposal of an 80% tariff on Chinese goods ahead of the talks underscored ongoing tensions, despite his administration outlining early negotiation targets spanning both major and minor trading partners. Market sentiment is characterized by volatility and reactive behavior to trade developments, with analysts expecting a protracted path to resolution. Treasury yields and the dollar also remained stable, despite a modest dip in the Bloomberg Dollar Spot Index. Bank of America’s Michael Hartnett predicted limited upside from here, noting that investors had already priced in optimism. Meanwhile, a Bloomberg Intelligence model signaled a downturn phase for the S&P 500, historically associated with weak returns.

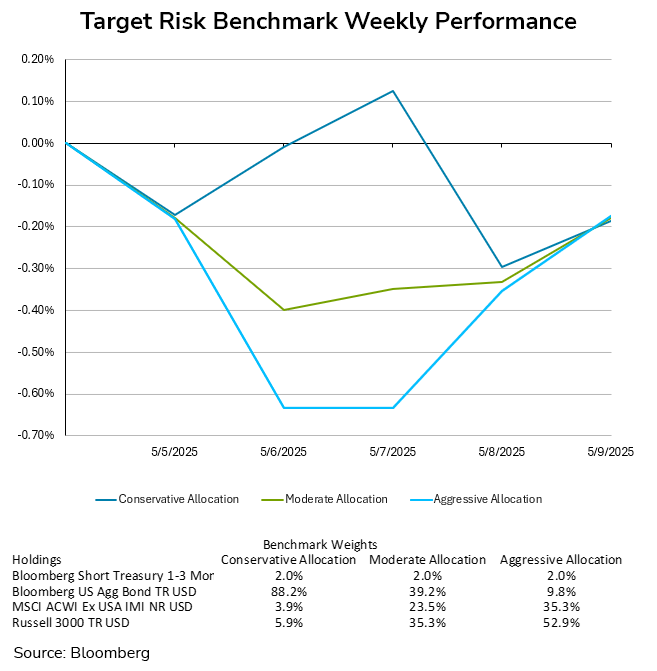

The sideways churn in markets for the week saw investors largely flat for the period across risk tolerances. After drifting downward to start the week, equities recovered ground, resulting in the aggressive target risk benchmark ending with a small loss of -0.17%. The moderate target risk benchmark finished in the same territory as well with a loss of -0.18%. The conservative target risk benchmark briefly saw a slight gain earlier in the week, but fell to end the week, with a similar weekly loss of -0.19%.

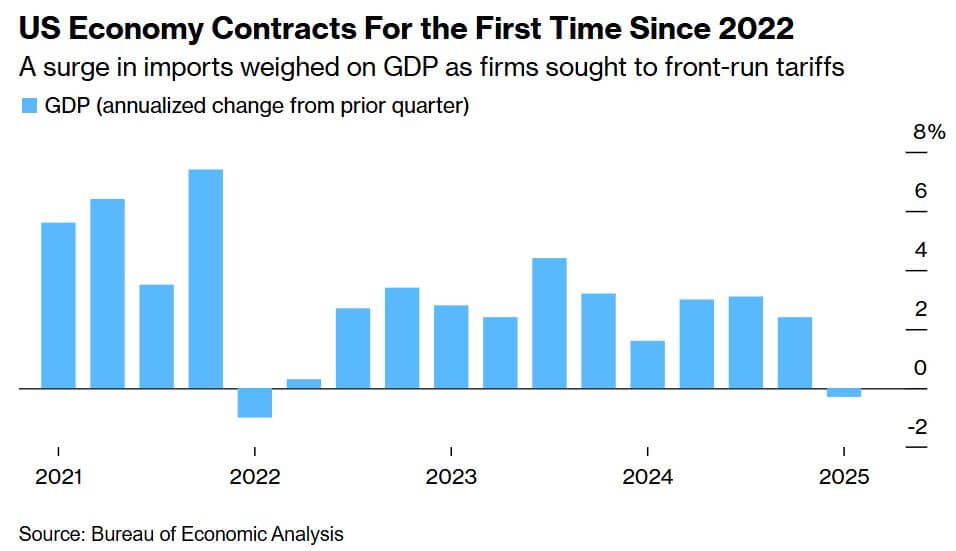

The U.S. economy contracted by 0.3% in Q1 2025, its first decline since 2022, driven by an unprecedented front-loading of imports ahead of new tariffs, which slashed nearly five percentage points from GDP via net exports—the sharpest drag on record. Despite this contraction, underlying domestic demand remained firm: consumer spending rose 1.8%, and business investment in equipment surged 22.5%, the fastest pace since 2020. Final sales to private purchasers, a core measure of domestic strength, climbed 3%. Inflation trends were favorable, with the core PCE index flat month-over-month in March for the first time in nearly five years.

The labor market exhibited continued resilience in April, adding 177,000 nonfarm payrolls, while unemployment held at 4.2%. Strength was concentrated in healthcare and transportation, while manufacturing shed jobs amid contracting output. Labor force participation rose to 62.6%, with prime-age engagement at a seven-month high. Wage growth moderated to 0.2% monthly and 3.8% annually, indicating easing wage pressures. Government employment shrank for a third straight month, led by Department of Government Efficiency layoffs, which now threaten up to 500,000 jobs due to fiscal cutbacks.

The Federal Reserve, under Chair Jerome Powell, opted to hold interest rates at 4.25%–4.5%, emphasizing a cautious, data-dependent posture amid rising risks of inflation and unemployment. Powell acknowledged that tariff-driven inflation could prove persistent and reiterated the need for patience. The Fed remains focused on balancing its dual mandate, wary of reigniting inflation while growth falters.

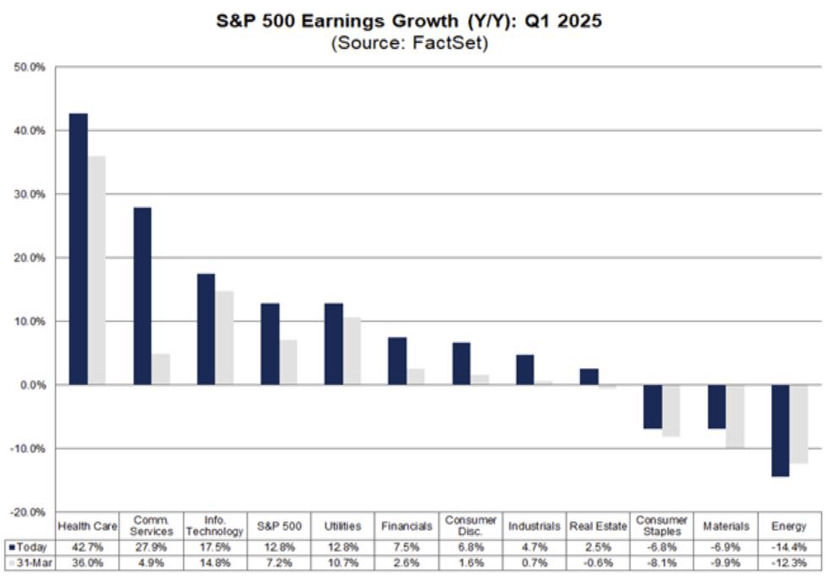

The Q1 2025 S&P 500 earnings season reveals a nuanced corporate backdrop marked by robust performance and growing caution. Companies have exceeded expectations with a 12.5% year-over-year EPS increase—up from a pre-season forecast of 6.6%—driven by strength in sectors like Health Care, Communication Services, Information Technology, and Financials. This is the second consecutive quarter of double-digit earnings gains and the seventh straight quarter of annual growth. Revenue trends, while positive, are more subdued. Only 62% of firms exceeded revenue expectations, and revenue growth stands at 4.8%, the 18th consecutive quarter of gains. Notably, the Industrials sector was the lone revenue decliner.

Despite this solid backdrop, forward guidance has deteriorated. Escalating tariffs and policy uncertainty have led major firms—including UPS and automakers—to withdraw forecasts. Recession mentions in earnings calls have surged, and analysts have revised Q2 2025 EPS estimates downward by 2.4%—a steeper cut than historical norms. Nine of eleven sectors saw declines, with Energy (-14.8%) leading the downgrades. Annual EPS forecasts for 2025 have also been trimmed by 3.1% since year-end, aligning with the 5-year average but exceeding longer-term trends. Sector-level weakness is most pronounced in Energy and Materials, while Communication Services has posted modest upward revisions. This divergence presents a “Rorschach test” for investors, with the data open to interpretation. Bulls can point to strong earnings momentum, while bears emphasize eroding guidance and macro risks. While not yet signaling an earnings recession, the outlook reflects rising vulnerability in an increasingly volatile policy environment.

For investors in U.S. equities, the current environment presents a challenging trade-off. While corporate fundamentals remain solid, there is growing concern they could weaken. In this context, hedged equity strategies may offer a balanced approach—providing exposure to potential market gains while helping to reduce downside risk. Freedom Investment Management offers a range of hedged equity solutions, including the Toews Managed Risk Blueprint and Swan Defined Risk strategies.

Alternatively, investors may consider sector rotation strategies, which aim to navigate shifting market conditions by reallocating among equity sectors to minimize risk and seize new opportunities. Freedom Investment Management provides access to several such strategies, including WestEnd Advisors U.S. Sector Model and Main Management Active Sector Rotation.