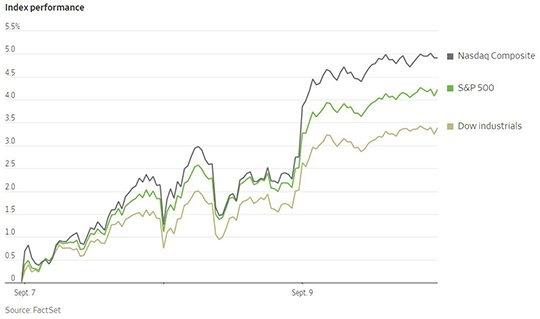

US stocks fought back to their first weekly gain in some time last week. That marked a welcome respite after three consecutive weeks of losses, triggered in part by Federal Reserve Chairman Jerome Powell’s unequivocally hawkish speech at Jackson Hole in August. Several indicators of investor sentiment had recently reached bearish levels, which generally suggest oversold conditions and are typically a contrarian buy signal. The Dow Jones Industrial Average rose 2.7% for the week, while the S&P 500 gained 3.6% and the Nasdaq Composite rallied by 4.1%. The gains in the S&P 500 were broad, with all 11 sectors appreciating for the week. Sectors that are sensitive to economic momentum had the most convincing gains, led by basic materials, consumer cyclical, and financials. US bond yields continued to rise last week, with the yield on the 10-Year US Treasury note touching 3.321% on Friday. US bond yields have now risen for the past six consecutive weeks and are within striking distance of the highs they reached back in June. Investors are now looking toward the next major economic data point on Tuesday with the release of the August Consumer Price Index data. Currently markets are pricing in another interest rate hike of 75 basis points by the Fed at its upcoming September policy meeting.

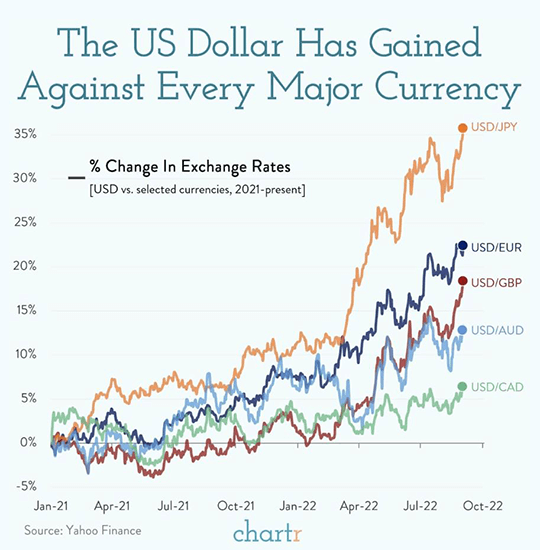

The US dollar has strengthened substantially against all major developed market currencies this year. The more aggressive path taken by the US Federal Reserve in tightening monetary policy in comparison to its foreign peers has been a significant contributing factor to USD strength thus far. During the month of August, the US dollar turned in the second-strongest performance among major global assets, trailing only the relentless surge in natural gas prices. The dollar currently stands at parity with the euro, marking the lowest relative valuation for the euro in two decades. British pound sterling last week touched its lowest valuation level relative to the USD since 1985. The UK is currently wrestling with sky-high energy prices and ongoing complications from Brexit. While the European Central Bank and the Bank of England have begun to hike interest rates as well, the Bank of Japan stands alone at this point in maintaining an easy monetary policy stance. The Japanese yen has been under significant selling pressure this year as a result, recently falling to a 24-year low versus the US dollar. It remains to be seen whether Japanese policymakers will continue their current policy stance or will be forced to pivot to support the yen. The strong dollar will help to ease inflation pressure in the US by making imports cheaper. However, it will also lower the value of foreign earnings by US multinational corporations and make US exports less competitive. Those challenges pale in comparison to the higher borrowing costs faced by foreign businesses and governments looking to borrow in US dollars, which will weigh on economic momentum outside the US.

The representations and opinions herein are the opinions and views of EQIS Capital Management, Inc. ("EQIS"), a registered investment adviser. The information is believed to be reliable but is not guaranteed by EQIS. The information contained herein is for informational and comparison purposes only and should not be relied upon as research or investment advice. When applicable, sources used in forming EQIS’s opinion are cited, however other sources may be available which contradict EQIS’s opinion, process and methodology. While EQIS believes the data to be reliable, no representation is made as to, and no responsibility, warranty or liability is accepted for the accuracy or completeness of such information. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future events. EQIS does not provide legal or tax advice.

LF1985