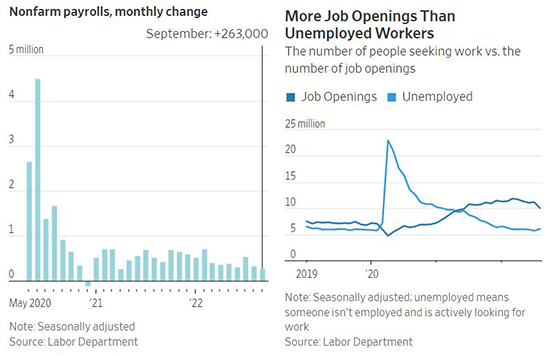

The US Labor Department released the September jobs report on Friday, which suggested that the US labor market cooled slightly but remains hot. US employers added 263,000 new jobs in September, a robust rate of job creation. This still was a welcome deceleration relative to the 315,000 jobs added in August. The unemployment rate unexpectedly dipped back down to 3.5% as the labor force participation rate decreased. That matches the 50-year low for the unemployment rate last touched in July. Wages rose by 5% in September compared to a year ago. This was a step in the right direction compared to August’s 5.2% increase in wages, but still a concerningly elevated reading. These data points mirrored the cooling trend shown by the August job openings report released earlier in the week. Total job openings fell by around 10% in August compared to the prior month to 10.1 million open positions. However, that is still much more than the 6 million people that were unemployed at that point. Altogether, the recent figures suggest that the labor market is beginning to loosen, but that there is still too much demand for labor relative to current supply. This reinforces expectations that the US Federal Reserve will raise interest rates again at its next policy meeting in November to reign in wages and inflation.

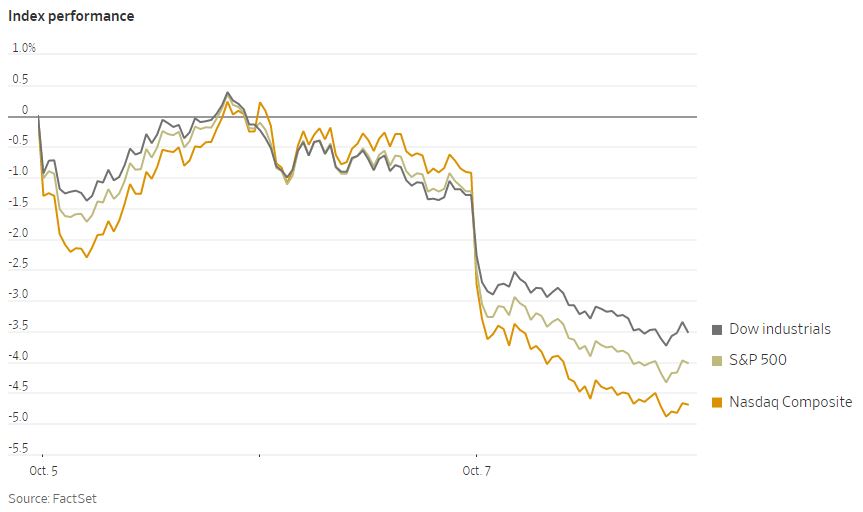

Equities rebounded from earlier losses to start the week, with the S&P 500 and Dow Jones Industrial Average recording their strongest two-day period since 2020 over Monday and Tuesday. However, over Wednesday and Thursday markets drifted lower following hawkish comments from Federal Reserve officials. Markets then sold off sharply on Friday in the wake of the jobs report. The Dow Jones Industrial Average fell 2.1% on Friday, while the S&P 500 lost 2.8% and the Nasdaq Composite fell 2.8%. However, the gains from earlier in the week were still sufficient for all three major US equity indices to hold onto gains for the week after three consecutive weeks of losses. The energy sector had by far the largest weekly gain at 11.13%, though basic materials, industrials and communication services all had weekly gains in the range of 2-3%. Derivatives markets now imply an 80% chance that the US Federal Reserve will raise the federal funds rate by 75 basis points again at the November policy meeting. That would be the fourth consecutive rate hike of 75 basis points. The yield on the 10-year US Treasury note rose to 3.89% on Friday. US bond yields have now risen for 10 weeks in a row, the longest continuous streak since the 1970s.