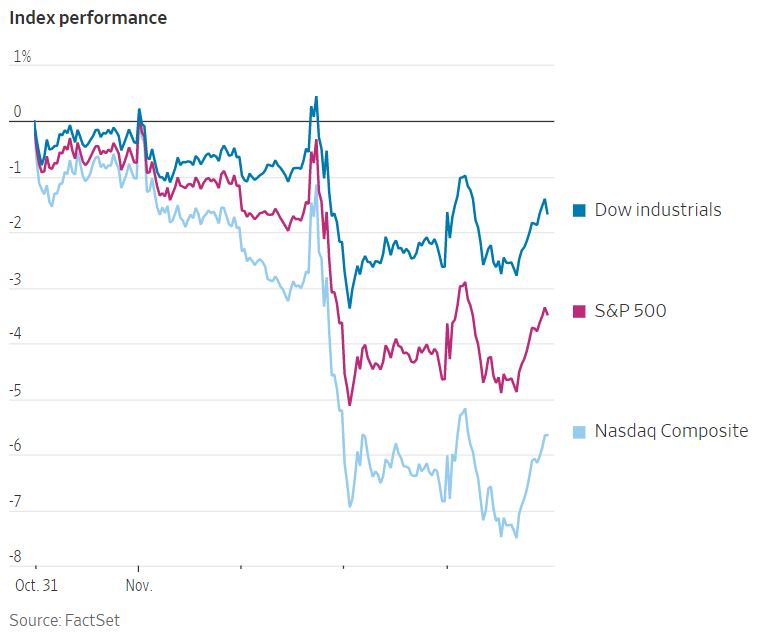

US stock indexes weathered another volatile week of trading as investors processed the most recent meeting of the US Federal Reserve. Despite a rally Friday, a hawkish tone from the Fed was a major factor in sending major US indexes to losses for the week. Notably, the Dow Jones Industrial Average snapped a weekly four-week winning streak. The materials and energy sectors of the S&P 500 notched moderate gains for the week, while technology and communication recorded weekly losses greater than 6%. The US 10-year Treasury note ended the week with a yield of 4.157%. The yield on the 10-year bond has now risen in 13 of the last 14 weeks. However, these significant moves were dwarfed by a dramatic selloff and recovery in Chinese markets over the last two weeks. The Hang Seng Index of Chinese stocks listed in Hong Kong sold off dramatically two weeks ago due to fears of the continuation of China’s COVID-zero policy, which has hamstrung economic activity. The Hang Seng then rallied back by 8.7% last week on mere speculation that these restrictive policies could ease, completing a round trip back to where they started.

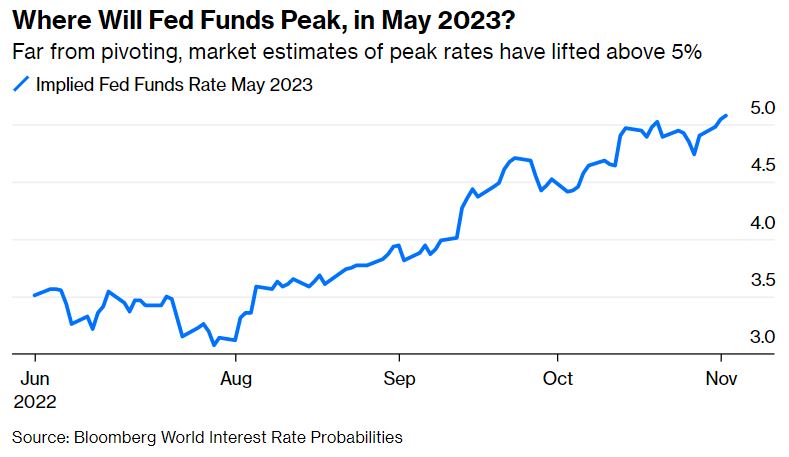

The US Federal Reserve increased its policy interest rate by 75 basis points last week, as was widely expected. This was the fourth consecutive rate hike of 75 basis points and puts the federal funds rate at a target range of 3.75% to 4%. The official statement issued by the Federal Open Market Committee (FOMC) formally acknowledged that it would consider the lagged effects of the cumulative rate hikes already enacted this year when evaluating future policy. This would imply the Fed may eventually slow the rate of interest rate hikes if the data permits, but stopped well short of committing to a dovish pivot as some market participants had optimistically speculated. Fed Chairman Jerome Powell emphasized in his following comments that even if the Fed does adjust the rate of hikes, the peak terminal rate is now estimated to be higher than it was previously. Interest rate futures markets reacted by pushing the implied peak terminal rate for May 2023 above 5% for the first time in this tightening cycle.

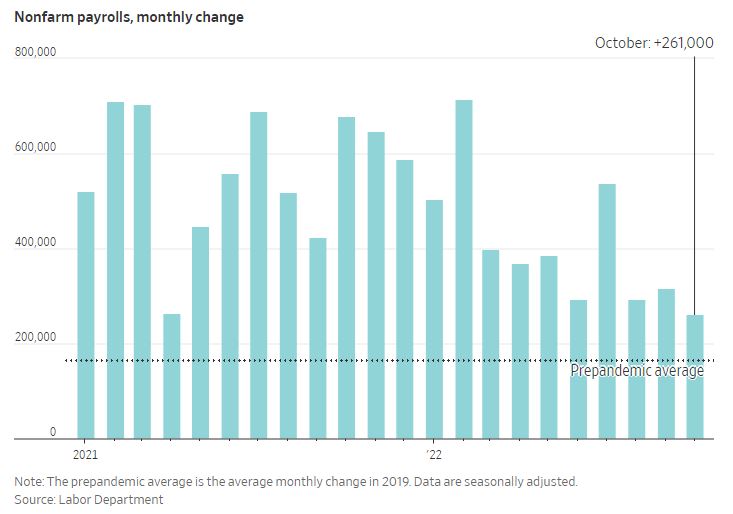

The first new data points on the state of the labor market last week generally showed continued strong demand for workers, though not quite at the extreme levels seen earlier in the year. Total job openings ticked back up in September to 10.7 million, an increase of 437,000 from the prior month. Though the total number of jobs in the economy has climbed back above pre-pandemic levels, areas of the service industry such as leisure and hospitality are still recovering, supporting continued demand for new hires. US employers added 261,000 new jobs in October, a level above economist estimates but lower than the month prior. The unemployment rate ticked up to 3.7% in a welcome sign of cooling for the Fed. Wage growth accelerated to 0.4% compared to the month prior, up from 0.3% in September. That equates to a 4.7% increase from a year ago. Looking at the third quarter overall, total compensation to civilian workers increased by 5% compared to a year ago. That is a lower increase than in the second quarter, but likely still too high for the Fed’s comfort. Following the data releases on the labor market, interest rate futures implied an interest rate increase of 50 basis points in December.