Several major US banks were among the companies to report fourth-quarter earnings last week, with Bank of America, Citigroup, Wells Fargo, and JPMorgan all beating analyst estimates for earnings for the quarter. So far, the increased interest income they received from higher interest rates from the US Federal Reserve has outweighed the slowing economy. Consumer spending remains strong, with credit card spending at those four banks up 10% relative to a year ago. However, consumers are not paying down their balances as quickly, with credit card balances rising 17%. That shows possible limits for future consumer spending power, though defaults remain low. The University of Michigan consumer sentiment survey rose to its highest level since April, showing Americans are more optimistic about the state of the economy. Consumer expectations for inflation one year from now also eased. Equities responded positively to these data points, with the Nasdaq Composite, S&P 500 and Dow Jones Industrial Average all recording gains of more than 2% for the week.

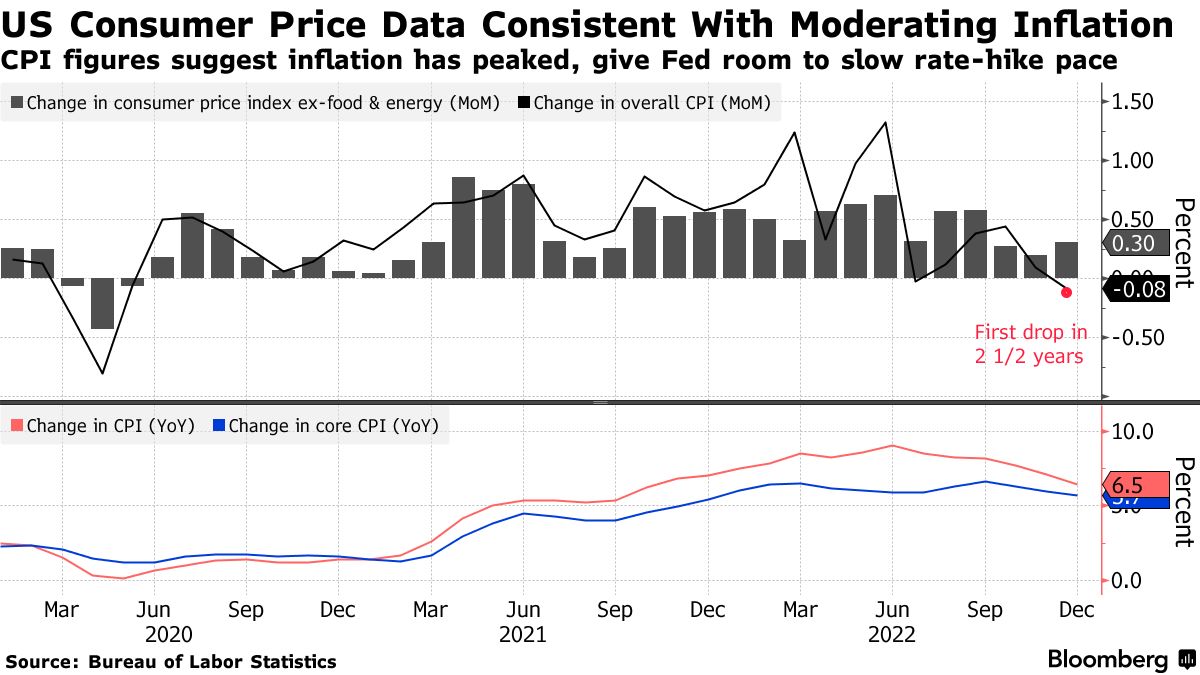

The Consumer Price Index (CPI) for December showed that US inflation continued to moderate for the sixth consecutive month since peaking in June. The CPI rose 6.5% last month compared to a year ago, in line with forecasts, while it fell 0.1% compared to the prior month, recording its first monthly decrease in 2 ½ years. Gasoline prices fell 9.4% last month and were the largest contributor to the cooler headline CPI figure. Core CPI, which excludes volatile food and energy prices, rose 5.7% compared to a year ago, its smallest increase in a year. Core CPI rose 0.3% compared to the prior month, also in line with economists’ forecasts. While goods prices continue to ease, services prices are still rising. This can be partially attributed to increasing shelter costs, which rose 0.8% in December. However, CPI calculates shelter costs with a lag, and more current indicators of rents show they are falling, decreasing the concern for that factor. The continuation of the easing price pressures may allow the Federal Reserve to downshift to an interest rate increase of 25 basis points at its next meeting in February.

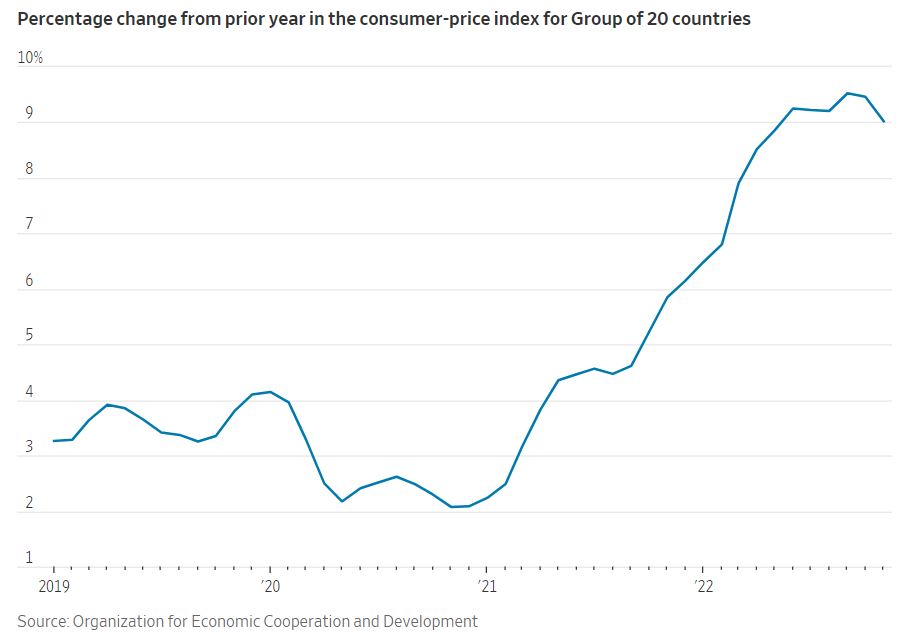

The World Bank last week released updated estimates for the global economy that were a sharp drop from prior projections. The World Bank now expects the global economy to grow by just 1.7% this year, in contrast to its prior estimate of 3% back in June 2022. The US economy is expected to grow 0.5% for the full year, narrowly avoiding recession. Though Europe looks set to avoid the worst-case scenario of a full energy crisis, the World Bank still expects no economic growth for the Eurozone in 2023. China is expected to bounce back later this year following its chaotic exit from zero-COVID with GDP growth of 4.3%. Meanwhile emerging markets are estimated to grow in aggregate at a rate of 3.4%. Meanwhile, the Organization for Economic Cooperation and Development (OECD) provided an unexpected source of good news last week. The OECD calculates inflation for the G-20 group of countries, which account for 80% of global economic output. In November, consumer prices for the G-20 rose by 9%. That represents the first slowdown in inflation since August 2021. That is a welcome first step in the right direction for global central banks’ fight with inflation.