Equity markets continued a winning streak as all three major indices finished last week in positive territory. The S&P 500, Dow Jones Industrial Average and Nasdaq gained 2.5%, 1.8%, and 4.3%, respectively. Investors appear to have renewed optimism as inflation is turning a corner, and the broader economy is not deteriorating as quickly as many forecasted. Investors will be keeping a close eye on the Federal Reserve’s meeting next week and expecting a less aggressive rate hike. The recent readings in inflation combined with the equity markets upward momentum have led investors once again into riskier corners of the market.

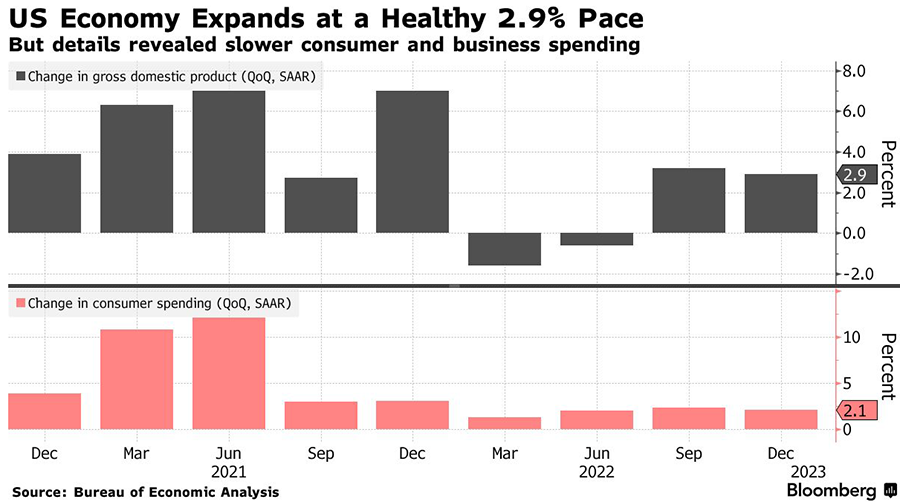

The US economy saw a slight slowdown in the fourth quarter of 2022, with GDP growth coming in at an annualized rate of 2.9%, according to data released by the Commerce Department. This still exceeded expectations, as economists had predicted a growth rate of 2.5%, but was a slower rate of growth than the third quarter’s expansion of 3.2%. Consumer spending grew at a solid annual pace of 2.1% last quarter, though that was short of forecasts. However, retail sales fell in December, suggesting that future consumer spending may soften. The broader measure of final sales to private domestic purchasers, which measure both consumer and business spending, slowed markedly to a 0.2% annual rate in the fourth quarter. That is a significant decrease from the third quarter’s growth rate of 1.1%. Meanwhile, the Commerce Department reported on Friday that US households decreased spending by 0.2% in December, as consumers continued to cut spending on goods but increased spending on services. The personal consumption expenditures index (PCE), the US Federal Reserve’s preferred measure of inflation, also increased at a slower pace in December, rising 5% compared to a year ago, a slowdown from the 5.5% increase in November. The core PCE index, which excludes volatile food and energy prices, rose 4.4% in December. That is a decrease compared to November’s 4.7% rise and is also the slowest rate of increase since October 2021. These data points make it more likely that the Fed will slow its pace of interest rate hikes to 25 basis points at its next meeting concluding on February 1st.

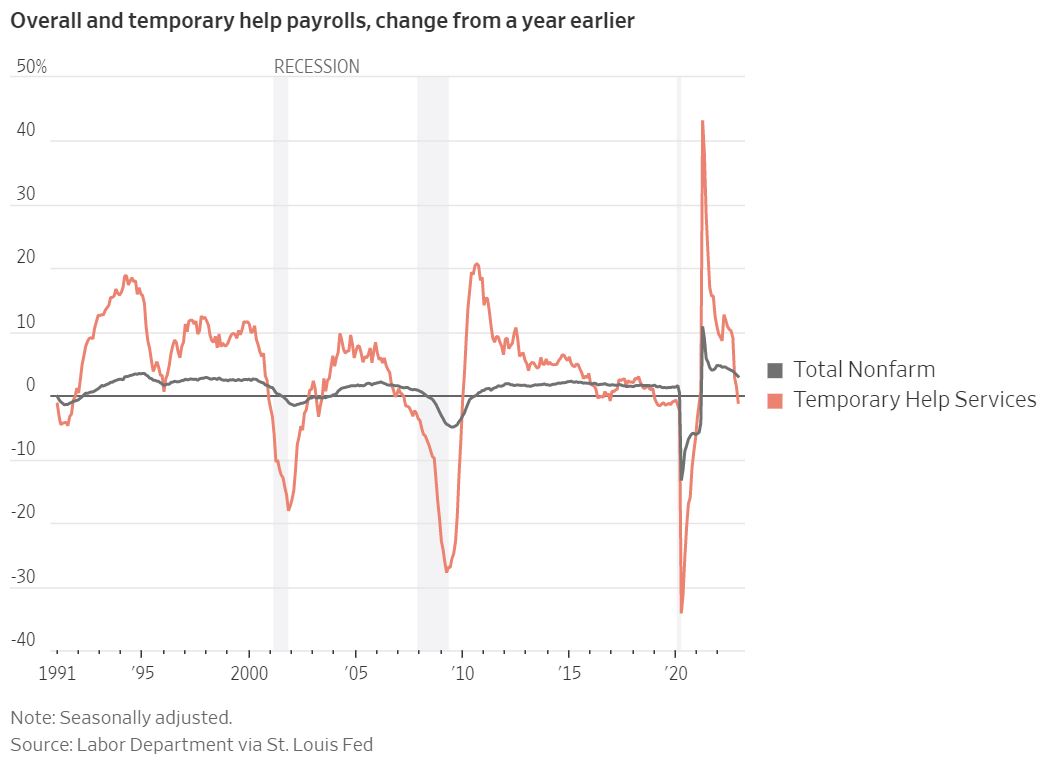

The labor market in the United States is still uncomfortably strong for the US Federal Reserve, with the unemployment rate at a 50-year low of 3.5% in December. In fact, initial jobless claims actually fell last week to a seasonally adjusted 186,000. However, companies are cutting back on the use of temporary workers, which is often seen as a leading indicator of economic activity. Temporary workers are much easier to hire and let go than permanent workers, and thus are often the first to be laid off. Over the last five months of 2022, employers let go of 110,800 temp workers. That trend has been accelerating, with 35,000 temp workers being laid off in December alone. Decreases in employment for temporary workers preceded layoffs for permanent workers in both the recessions of 2001 and 2007-09. This trend is being echoed in the experiences of unemployed Americans, who are finding that job searches are taking longer than in the past. Many unemployed workers are reporting that they are having difficulty finding new jobs, even in industries that were previously considered to be strong, such as healthcare and technology. Last spring, unemployed workers that had been looking for a job for 3.5 to 6 months totaled 526,000, a half-century low. Last month, that figure had risen to 826,000 unemployed workers, an increase of 26%. Though that may be bad news for those unemployed workers, that may indicate that wage pressures will ease in the coming months. That would be good news for inflation and the path of US interest rates this year.