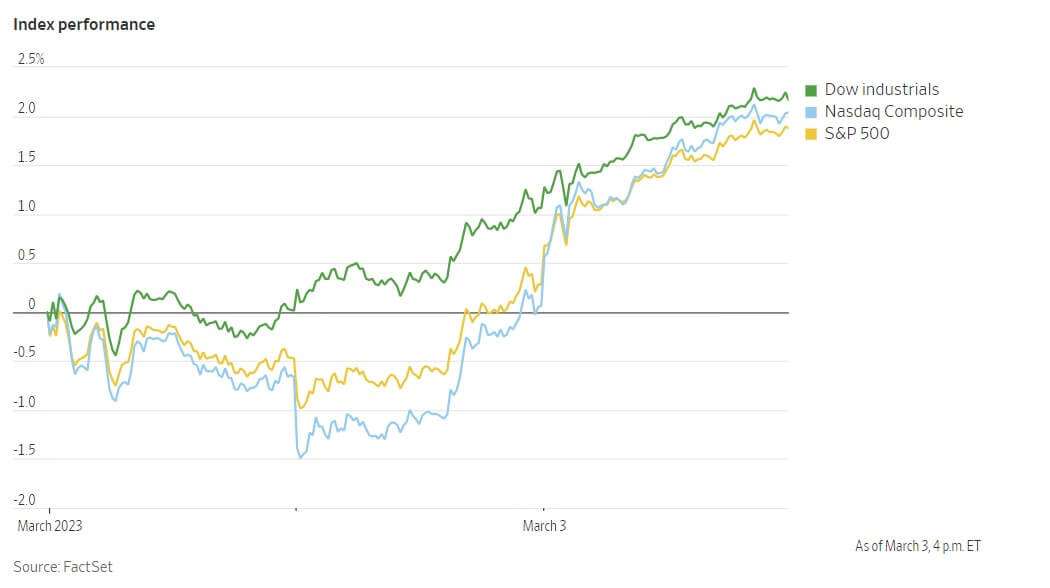

U.S. stocks rebounded last Friday after data showed strong activity in the U.S. services sector, outweighing concerns about inflation and global monetary policy tightening. The S&P 500 rose 0.7%, the Nasdaq Composite added 1.6%, and the Dow Jones Industrial Average gained 1%. Stocks were fluctuating all week due to strong global economic data boosting inflation expectations, leading central banks to consider raising interest rates. Two readouts on the U.S. services sector released on Friday showed relatively robust spending in February. The S&P Global U.S. Services PMI index rose to 50.6, the highest reading since June, and the Institute for Supply Management’s services activity index exceeded the consensus forecast of economists. Despite this positive economic data, the yield on the benchmark 10-year Treasury note continued to rise, reflecting bond traders’ growing expectations that the U.S. Federal Reserve will maintain a hawkish bent on interest rates to tame inflation.

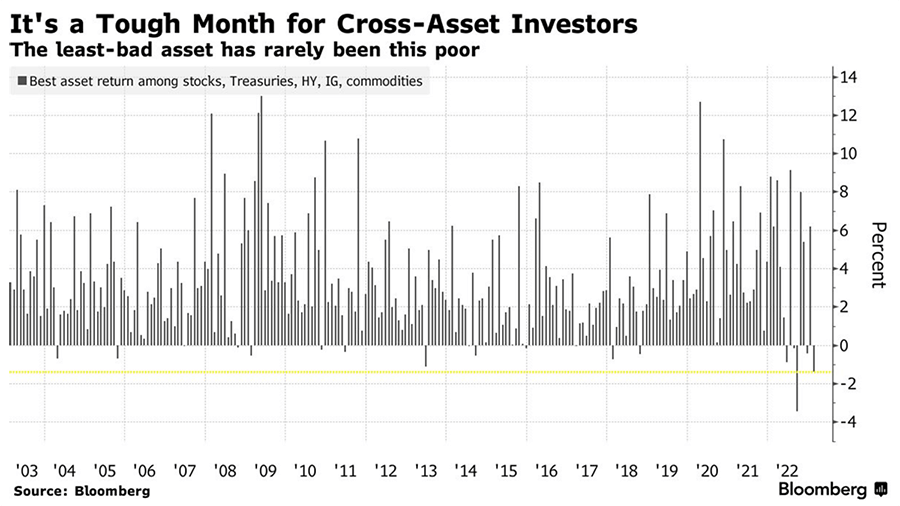

Investors experienced a reversal of January's rally as bets on cooling inflation and lower rates proved misplaced in February. From stocks to fixed income and commodities, almost every asset class saw declines. The “best” return among major US assets was a decline of 1.4% through Monday from high-yield bonds. That was followed by a drop of roughly 2.5% each in Treasuries and the S&P 500 Index, a 3.2% slide in investment-grade bonds and a 5% slump in commodities. The pervasiveness of losses was notable, with only one other month in the past four decades seeing the best return among asset classes come in worse than this one. The post-pandemic market has been characterized by all-or-nothing stakes, with almost every asset linked to the trajectory of economic news and central bank policy. The stronger-than-expected economic data forced traders of all stripes to back away from expectations that major central banks around the globe are close to finished with monetary tightening. The shift in policy expectations hit the fixed income market, with two-year Treasury yields jumping to the highest level since 2007. The yield curve between two-year and 10-year Treasuries inverted to levels not seen in four decades. While stronger data, particularly in the US labor market, eased concern about an imminent recession, that risk still lingers. The S&P 500 fell for three straight weeks, with February’s decline wiping out almost half of the previous month’s advance. Even commodities, often touted as a hedge for inflation, couldn’t escape the pull from higher rates. As earnings season ends, investors will be more driven by economic data in the coming weeks.

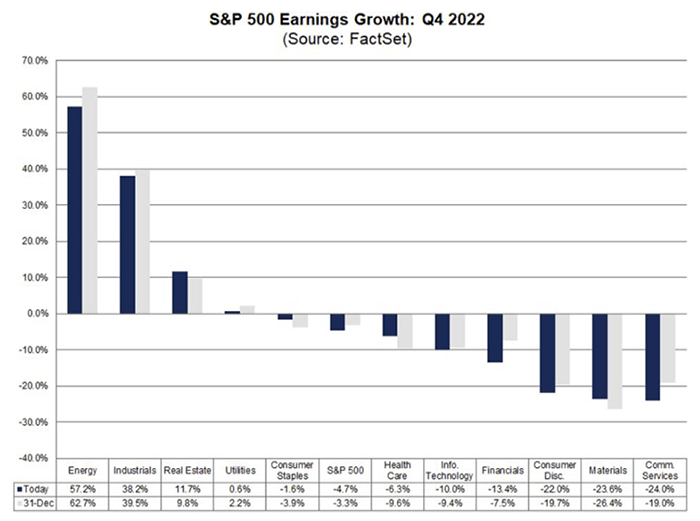

With 82% of S&P 500 companies having reported their Q4 2022 earnings so far, aggregate earnings have beaten estimates by just 1.3%. That is lower than the 1-year average (+3.7%), 5-year average (+8.6%), and 10-year average (+6.4%). This marks the seventh consecutive quarter in which the EPS surprise percentage for the index has decreased. This is due to overestimated earnings for companies in specific sectors and industries, resulting in fewer companies beating EPS estimates than average. Communication Services (-4.1%) and Consumer Discretionary (-0.4%) are currently reporting a negative earnings surprise percentage for Q4 2022, with Alphabet and Facebook contributing to the negative surprise for the Communications Services sector, and Amazon.com contributing to the negative surprise for the Consumer Discretionary sector. Other companies, such as Apple, Boeing and Goldman Sachs, have also reported negative EPS surprises, lowering the overall EPS surprise percentage for the index.

The S&P 500 is reporting a larger earnings decline (-4.7%) than expected at the end of the quarter (-3.3%) due to the lower earnings surprise percentage and continued downward revisions to EPS estimates. However, the market is punishing S&P 500 companies that report negative EPS surprises for Q4 less than average, showing that macroeconomic factors such as inflation and interest rates are currently having a larger influence on equity performance than fundamentals. Looking ahead, analysts expect earnings declines for the first half of 2023, but earnings growth for the second half of 2023. For Q1 2023 and Q2 2023, analysts are projecting earnings declines of -5.4% and -3.4%, respectively. For Q3 2023 and Q4 2023, analysts are projecting earnings growth of 3.3% and 9.7%, respectively. For all of CY 2023, analysts predict earnings growth of 2.3%.