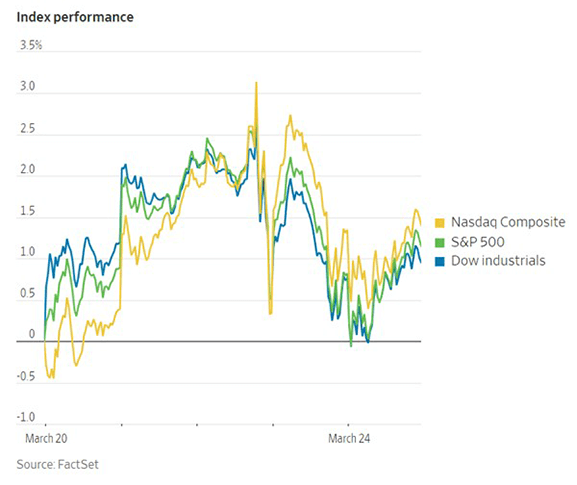

All three major indexes finished last week in positive territory as the Nasdaq closed up 1.66%, the S&P 500 up 1.39%, and the Dow Industrials up 1.18%. Treasuries rallied and the dollar index was up 0.6%, with gold and bitcoin futures down. WTI crude settled down 1.0% but was still up 3.8% for the week. Concerns about uninsured deposits and bank borrowing from the Fed's backstop facilities remained elevated, while the March S&P US Flash manufacturing and services PMIs beat expectations. February US durable goods orders posted a surprise contraction, and Fed commentary indicated that while a recession is not the base case, regulators are ready to take further actions should the bank crisis worsen.

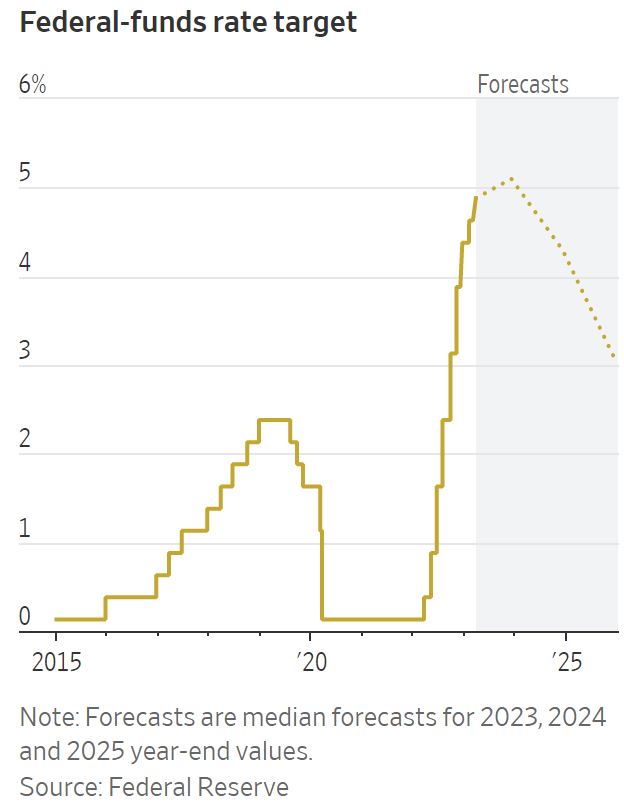

The US Federal Reserve raised interest rates for the ninth time in a year last Wednesday, increasing the benchmark federal-funds rate by a quarter percentage point to a range of 4.75% to 5%, the highest level since September 2007. However, the central bank indicated that banking-system turmoil might bring an end to its rate-rise campaign sooner than expected and dropped a phrase from previous policy statements that had indicated “ongoing increases” in rates would be appropriate. Instead, the statement shifted to the less hawkish phrase of "some additional policy firming may be appropriate." The updated Fed dot plot showed that 17 out of 18 officials estimate that the fed-funds rate would remain above 5.1% at year end, implying one final quarter-point increase was still likely. The statement noted that the banking system remained sound and resilient, but there were concerns that recent developments could result in tighter credit conditions for households and businesses, and slow economic activity, hiring and inflation. The upheaval in the banking system demonstrated the potential spillover from higher interest rates to the economy as a whole, the statement noted. The fed-funds rate influences borrowing costs throughout the economy, including rates on mortgages, credit cards and auto loans. The Bank of England matched the Fed in hiking by 25 basis points on Thursday, bringing its key interest rate to 4.25%. The European Central Bank also raised its policy rate by 50 basis points the preceding week.

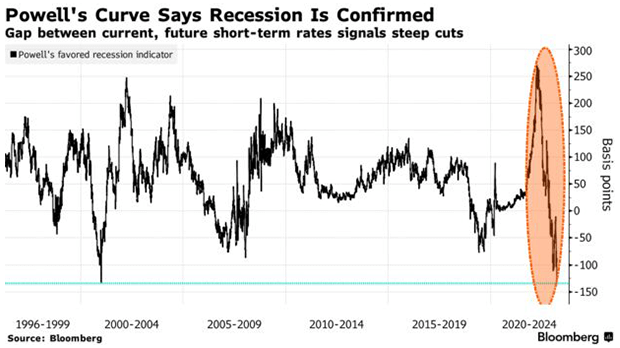

The bond market metric highlighted by Federal Reserve Chairman Jerome Powell a year ago is indicating that a recession is likely to occur in the US, along with rate cuts later this year. Powell has previously highlighted the historical accuracy of an inversion in the first 18 months of the yield curve in forecasting recessions. The expected three-month T-bill rate in 18 months’ time has dropped to 134 basis points below the current rate. That is below its previous record nadir, which occurred two months before the US economy fell into recession in January 2001. Treasury yields rallied after the Fed raised its benchmark rate by a quarter point, with traders increasing their bets that the central bank will start cutting interest rates soon. This view contrasts with the Fed's guidance that it expects to raise rates at least once from here, and with Powell's comments that he does not expect any reductions to borrowing costs this year. TD Securities strategists predict that the Fed will have to cut rates more quickly than the market currently anticipates, as the economy slides into a recession in Q4. Swaps traders see a 50% chance that the Fed will not raise rates again. The inverted part of the yield curve, which is often a recession indicator, has climbed back above zero just before the onset of an economic contraction in the past.