US stocks made a modest recovery from earlier losses to end the shortened trading week, with the S&P 500 rising 0.4% and the Dow Jones Industrial Average remaining flat. The Nasdaq Composite climbed 0.8%. The recent trading pattern has been marked by little momentum in either direction following the previous week's substantial gains, and investors are cautiously optimistic that the strains in the banking sector will not lead to a full-blown crisis. However, recent data have provided cause for concern about the economic outlook. The latest data showed that new jobless claims were higher than previously thought, raising fears of a cooling labor market, though that may be welcome news for the Federal Reserve’s fight against inflation. Investors are also uncertain about the mixed signals sent by economic reports, making it difficult to determine if the economy is in good shape or heading towards a recession. Meanwhile, the yield on the benchmark 10-year US Treasury note was little changed at 3.3%, reflecting a run of lackluster data that has caused investors to bet that future interest rates will not be as high as previously expected. In Europe, the Stoxx Europe 600 gained 0.5%. Hong Kong’s Hang Seng gained 0.3%, while Japan’s Nikkei 225 fell 1.2%. South Korea’s Kospi lost 1.4%.

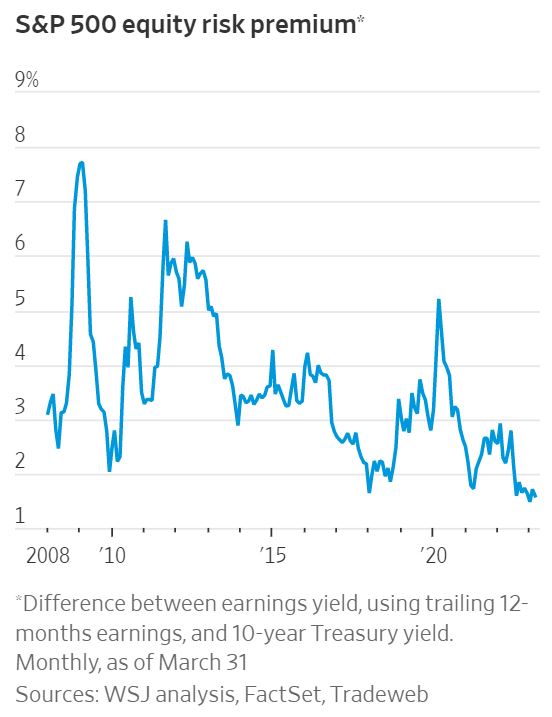

The reward for owning stocks over bonds is currently at a record low since before the 2008 financial crisis, according to the gap between the S&P 500’s earnings yield and the yield of 10-year Treasuries. This measure of the equity risk premium currently stands at 1.59%, well below the average gap of around 3.5% since 2008. This is a challenge for stocks, as they need to offer a higher reward than bonds to attract investors due to their higher volatility. The reduction in the equity risk premium has been caused by bond yields rising and the earnings yield of equities falling, which can occur due to weaker earnings or higher stock prices. While some analysts predict that the peak for stock market valuations has been reached, this does not necessarily mean that peak prices have been seen yet in this cycle. Analysts expect earnings for companies in the S&P 500 to edge up roughly 1.6% in 2023, according to FactSet. While certain sectors of the equity market may look pricey, some investors say value stocks, which trade at cheaper valuation multiples, may warrant consideration. While value stocks outperformed growth last year, that relationship has reversed YTD. The Russell 3000 Growth Index has gained 12% so far this year, while the Russell 3000 Value Index has feen flat. Historically, when inflation was in the range of 4% to 8%, value stocks outperformed growth by 6% to 8% on an annual basis.

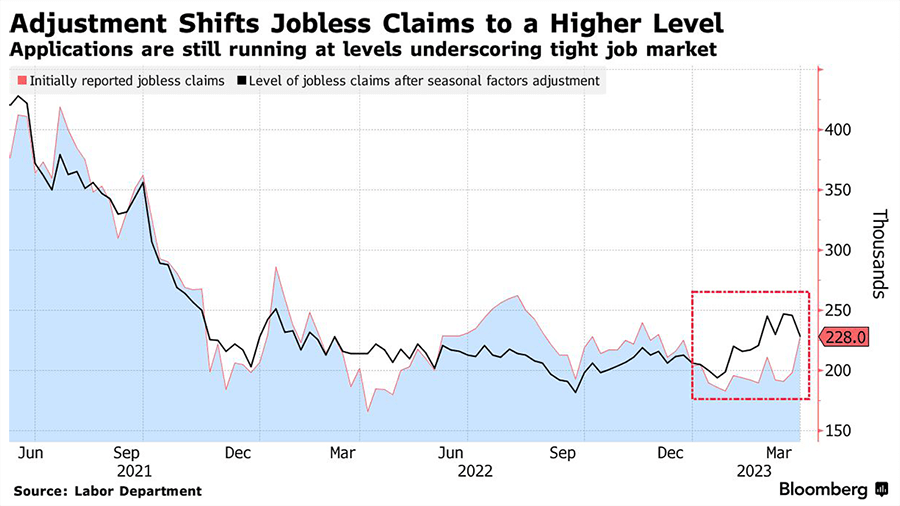

According to Labor Department data, initial unemployment claims in the US were 228,000 in the week ended April 1, exceeding almost all economists' estimates. This was partly due to revisions in data to adjust for seasonal factors, with the previous week's numbers being revised up by 48,000 to 246,000. The revised data provides a more accurate picture of claims levels and patterns for both initial and continued claims, said the report. Continuing claims, a good indicator of how hard it is for people to find work after losing their job, was little changed at 1.82 million in the week ended March 25. Despite economists being puzzled as to why claims were so low, applications are still relatively low and indicative of strong demand for workers. The higher level of claims shouldn't be interpreted as a sign that layoffs have suddenly surged, according to Santander US Capital Markets. The four-week moving average in initial claims fell to 237,750 from an upwardly revised 242,000 in the prior period. On an unadjusted basis, claims fell by around 17,000 to 206,931. Separately, a report from Challenger, Gray & Christmas showed job-cut announcements from US-based employers rose 15% in March from the prior month.