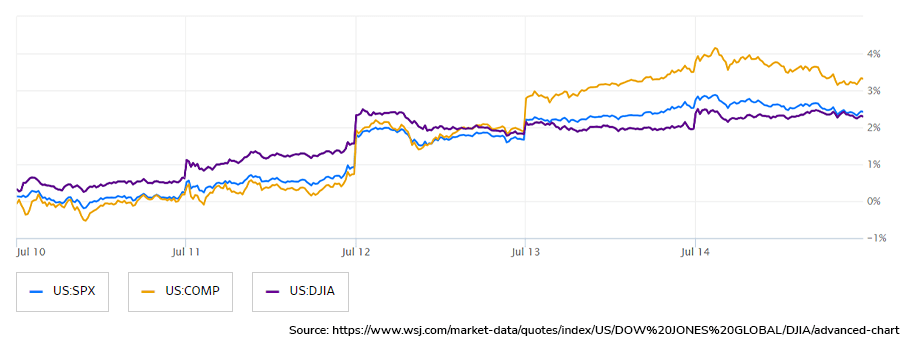

Major stock indexes saw gains last week as earnings season began with reports from major banks. JPMorgan reported a profit of over $14 billion, surpassing expectations, while Wells Fargo and BlackRock also saw an increase in earnings. Although Citigroup's profit declined, it still exceeded analysts' forecasts. JPMorgan and Wells Fargo shares rose, outperforming the falling bank-stock index, while State Street, a trust bank, saw a drop. Earnings season coincided with optimism about the U.S. economy and signs of cooling inflation, which have bolstered stock performance in recent days. Equity strategists have been raising earnings forecasts for the S&P 500, indicating optimism for the profit outlook.

However, concerns about inflation, policy tightening and potential risks of a recession or Federal Reserve policy error remain. On Thursday, the S&P 500 reached its highest close since April 2022, while at the end of the week it declined slightly, ending a four-day rally. However, the Dow Jones Industrial Average rose by 0.3% (over 100 points), while the Nasdaq Composite saw a 0.2% decrease. The bond market saw reversals as strong economic data suggested it might be too early for the Federal Reserve to declare victory over inflation. Consumer sentiment reached a nearly two-year high and short-term price expectations rose, leading to selling in bonds, particularly in the short-term end of the US curve. Yields on U.S. government bonds saw a slight increase after declining on Thursday, with the yield on the 10-year Treasury note reaching 3.818% on Friday, compared to 3.759% on Thursday. The WSJ Dollar Index showed a small upward movement, halting a six-day slide that had taken it to its lowest level since February. In other markets, emerging-market currencies experienced their best week since January. The cryptocurrency market saw a decline, with Bitcoin falling 4% and Ether dropping 3.5%. Oil prices managed to rise for a third consecutive week, although Brent crude, the international oil benchmark, experienced a 1.8% decline on Friday, settling around $80 per barrel.

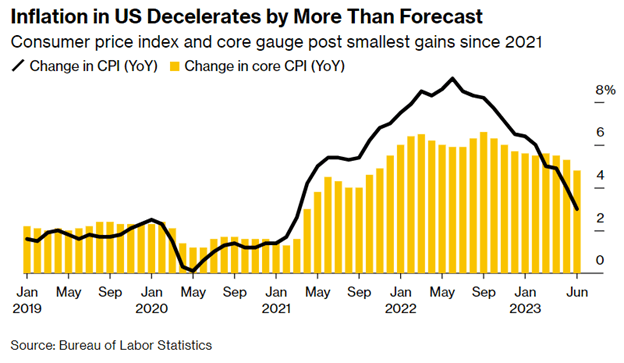

The latest report from the Labor Department indicated that U.S. inflation eased to its slowest pace in over two years, with underlying price pressures moderating more than expected. In June, the consumer price index (CPI) rose by 3% compared to the previous year, significantly lower than the peak of 9.1% in June 2022 and down from 4% in May. The report also highlights that core consumer prices, which exclude volatile food and energy categories, rose by 4.8% in June compared to the previous year, marking the slowest pace since October 2021 and a decrease from 5.3% in May. Economists had initially estimated a 5% increase in core prices, making this decline notable.

Although this represents a positive development, inflation still remains above the Federal Reserve's target of 2%. In response to signs of stronger-than-anticipated economic activity, Federal Reserve officials have signaled their intention to raise interest rates to a 22-year high at their upcoming meeting on July 25-26. The recent inflation report is unlikely to change this course of action. During the June meeting, officials maintained the benchmark federal-funds rate between 5% and 5.25%, marking the first pause after 10 consecutive rate increases since March 2022. Most officials present at the prior meeting projected two more rate hikes to occur later this year. Federal Reserve officials remain focused on addressing stubbornly high core inflation, considering it a better predictor of future inflation than the overall rate. The Labor Department's report may strengthen the case of officials who believe that the central bank has taken sufficient measures to contain price pressures and that it should allow the cumulative effects of previous rate increases to take effect. The implied chances of an additional Fed rate increase after this month slipped to well below 50% following the release of the June CPI data.

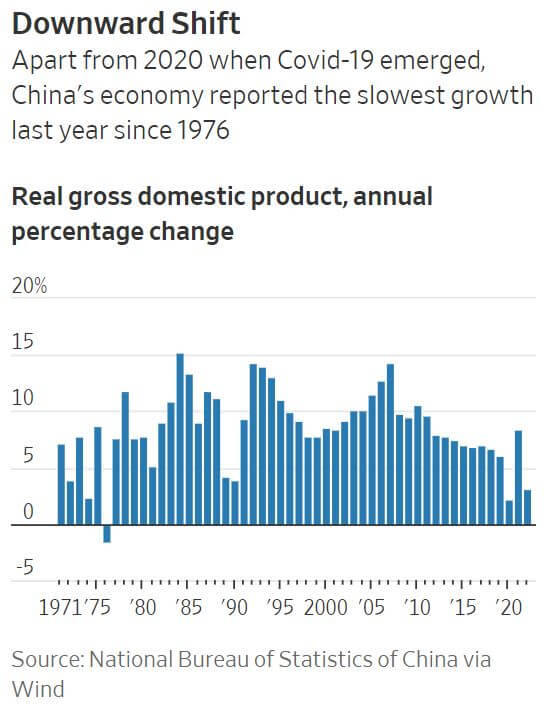

China's headline economic growth appears solid compared to many other countries, but the situation on the ground feels more like a recession. Negative sentiment among businesses and job seekers stems from a combination of factors, including the economic slowdown, the impact of COVID-19, a downturn in the property market, and regulatory crackdowns on tech companies. While China hasn't officially entered a recession, its economic pain goes beyond the reported growth figures. The strength in GDP growth is mainly due to a favorable comparison with the previous year, which was heavily impacted by COVID-19 lockdowns. Quarter-over-quarter growth is expected to be modest. China is on the brink of deflation, with falling factory-gate prices and minimal consumer inflation. The country's exports have declined significantly, and youth unemployment has reached a record high. China's property sector, which initially showed signs of recovery, is now deteriorating again with falling prices in most markets. Private investment, a key driver of job creation, has turned negative for a sustained period.

Some economists suggest that China may be experiencing a "balance-sheet recession," characterized by heavy debts, low consumer and business confidence, and limited borrowing appetite. The slowdown in China's economy has global implications. As the US and other Western economies face their own risks of recession, a weak Chinese economy dampens demand for resources and affects multinational firms relying on the Chinese market. Despite some positive developments, such as significant investment in priority industries like semiconductors and becoming the largest auto exporter, the overall economic outlook remains uncertain. Chinese authorities have refrained from large-scale stimulus so far, opting for modest interest rate cuts and limited measures.