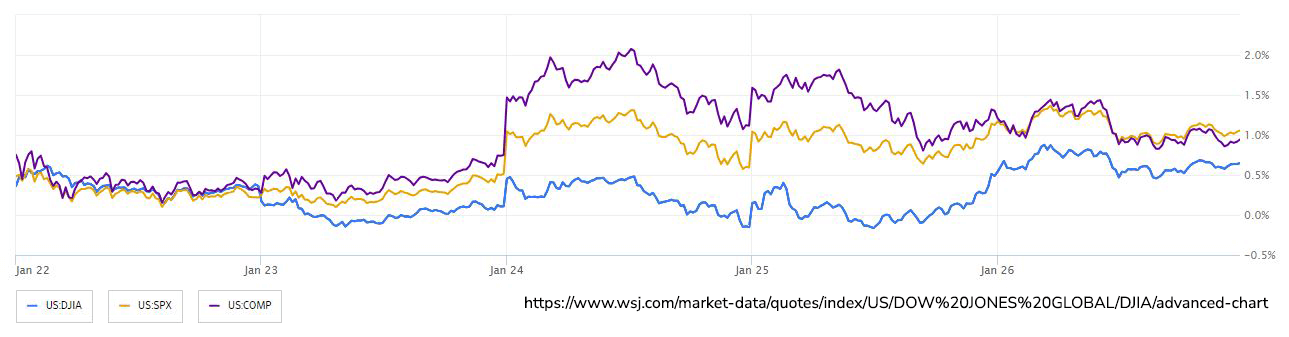

Wall Street experienced a decline in Treasury values last week as traders speculated that the Federal Reserve would exhibit patience before considering interest rate cuts later in the year. Shorter-maturity bonds led losses, driven by personal spending exceeding expectations, even as the Fed's preferred measure of underlying inflation slowed to a nearly three-year low. Investors haven't abandoned expectations for a first-quarter rate cut, but the focus has shifted to May, pending upcoming economic reports and the yet-to-be-seen impact of shipping disruptions. Two-year Treasury yields exceeded 4.35%, the S&P 500 held onto a third straight weekly gain, and the Nasdaq 100 underperformed due to disappointing forecasts from Intel and KLA. Oil prices reached a two-month high after a fuel tanker operated by Trafigura Group was struck by a missile, emphasizing geopolitical risks to crude supplies. The focus is on the upcoming Federal Open Market Committee (FOMC) meeting for a potential shift in rates, with expectations that the Fed may discuss a rate-cutting cycle. Powell and colleagues may take their time easing policy, focusing on a surprisingly steep drop in inflation rather than countering economic contraction. The ongoing fourth-quarter earnings season is considered crucial for the equity market's direction in 2024. Earnings for companies in the S&P 500 outside of Nvidia, Amazon, Meta, Alphabet, Microsoft, and Apple are expected to decline 10.5% for the quarter. Including those six companies limits expected fourth quarter losses to 1.4%. Tesla meanwhile has deviated from the other technology giants and has fallen more than 25% over the last four weeks after badly missing analyst revenue and earnings targets for Q4.

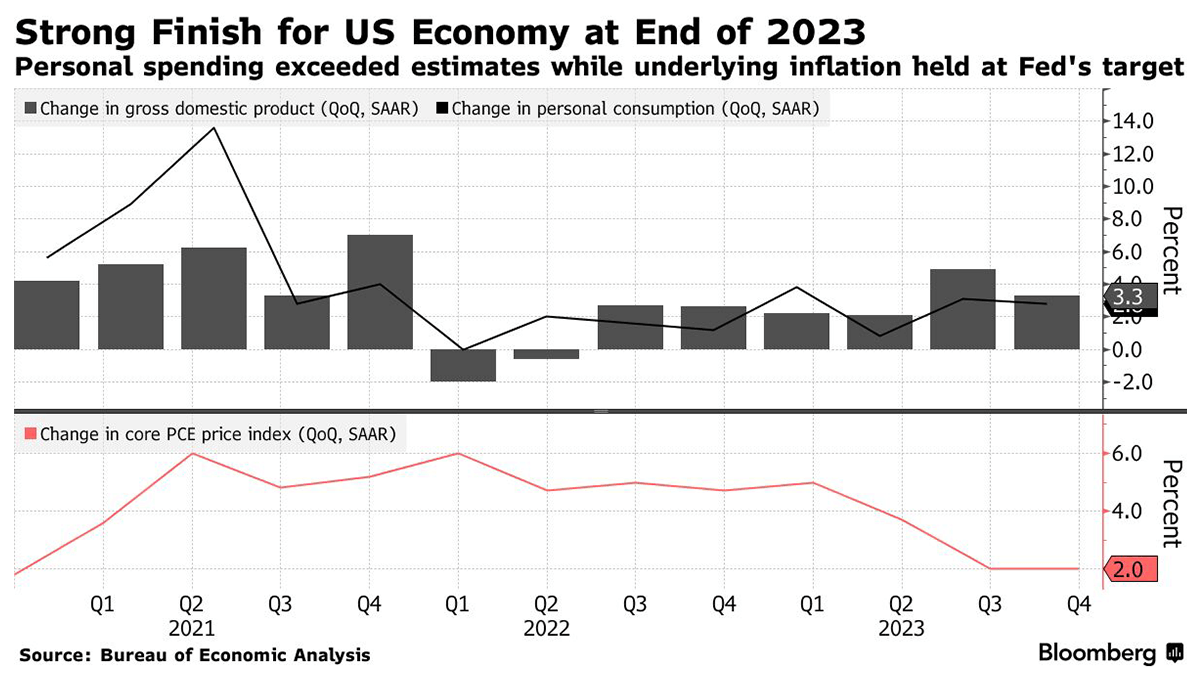

The U.S. economy demonstrated unexpected resilience in 2023, growing at a rate of 3.1% over the year, confounding earlier projections of a looming recession. The Commerce Department last week reported a surprising 3.3% growth in the fourth quarter, though lower than the summer's robust 4.9% pace. The credit for the better-than-expected growth is attributed to consumers who sustained spending on various fronts, including healthcare, dining out, and cars. Meanwhile, the Federal Reserve’s preferred measure of inflation, the personal consumption expenditures (PCE) index, rose 2.6% compared to a year ago in December. The core PCE index, which excludes food and energy costs, rose 2.9% compared to a year ago. The six- month annualized core PCE rate increased by 1.9% over the second half of the year, consistent with the Fed’s 2% inflation target. Economic growth is set to continue in 2024, albeit at a slower pace, supported by an expected Federal Reserve pivot toward interest-rate cuts, moderating inflation, and a strong labor market. Falling mortgage rates are already contributing to increased housing activity, following a challenging year for home sales. However, there are indications that the economy may not sustain such rapid growth. Economists foresee a cooling of consumer outlays, projecting a growth rate of 1% for the current year. Concerns arise from signs such as increasing credit delinquency rates, a decline in the personal saving rate to 4%, and consumers relying on debt to support spending. Despite the overall positive economic outlook, there are signs of a slowing economy, with manufacturing firms reporting a modest drop in production, some large firms announcing layoffs, and certain sectors facing challenges in maintaining pricing power. The prospect of the Federal Reserve lowering interest rates has fueled optimism in the stock market, with expectations that cheaper financing costs could stimulate household spending and business investment.

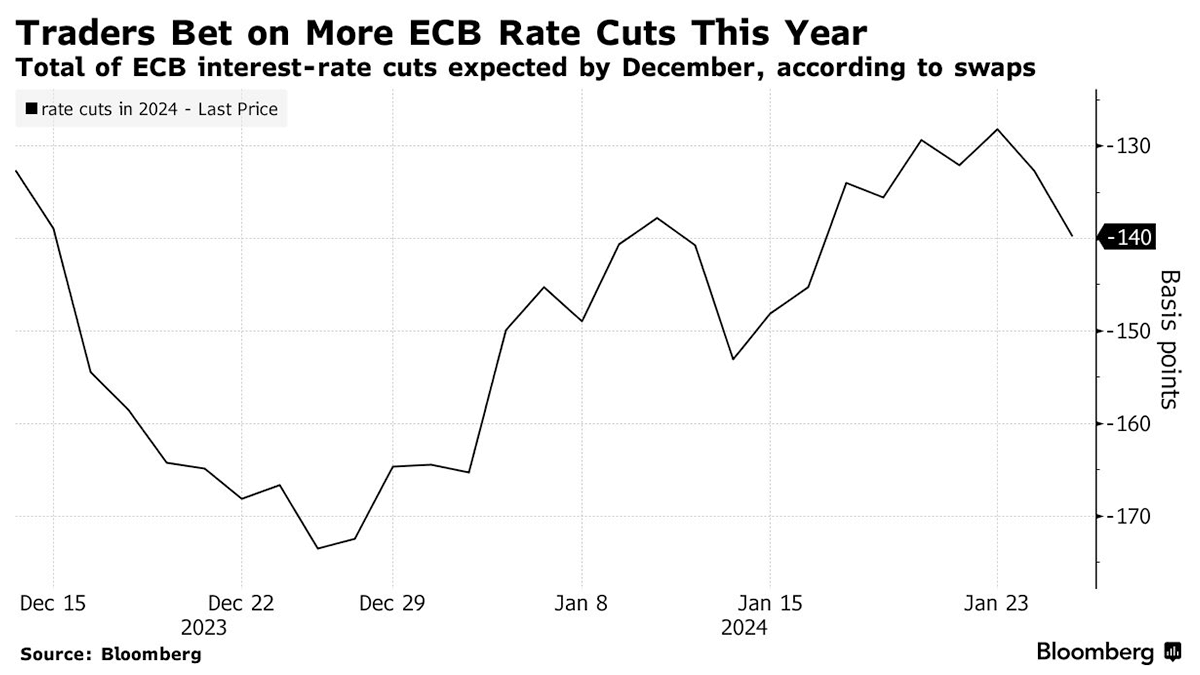

The European Central Bank (ECB) maintained its key interest rate at a record high last week, but ECB President Christine Lagarde left the possibility of rate cuts open, suggesting they might occur as early as spring. Following a series of aggressive interest rate increases, investors are closely monitoring the timing and pace of potential rate cuts, influenced by global central banks signaling a shift towards rate reductions amid easing inflation. Lagarde, in a news conference, acknowledged the market's anticipation of rate cuts in April but stated it was premature to discuss such measures. Lagarde highlighted a slight decline in wage growth in the eurozone, a crucial metric for the ECB's fight against high inflation. While the ECB decided to maintain its deposit rate at 4%, Lagarde's comments led to a rally in European stock markets and a decline in yields on eurozone government debt, suggesting investor expectations of lower borrowing costs. The euro also depreciated against the dollar. Average investor expectations, based on Refinitiv data, indicate an anticipated reduction of around 1.34 percentage points in ECB rates this year, starting possibly in April. The economic backdrop in Europe has been stagnating for over a year, with various challenges impacting the export-focused business model, including slower growth in China, higher energy prices, global trade tensions, and the costly transition to green energy. Lagarde's ECB is cautious about potential risks that may reinforce inflation, such as persistently low unemployment, wage pressures, and supply shocks. The ECB and other central banks are cautious about a premature rate cut, fearing a relapse in inflation, particularly as they approach the challenging task of moving from 3% to 2% inflation.