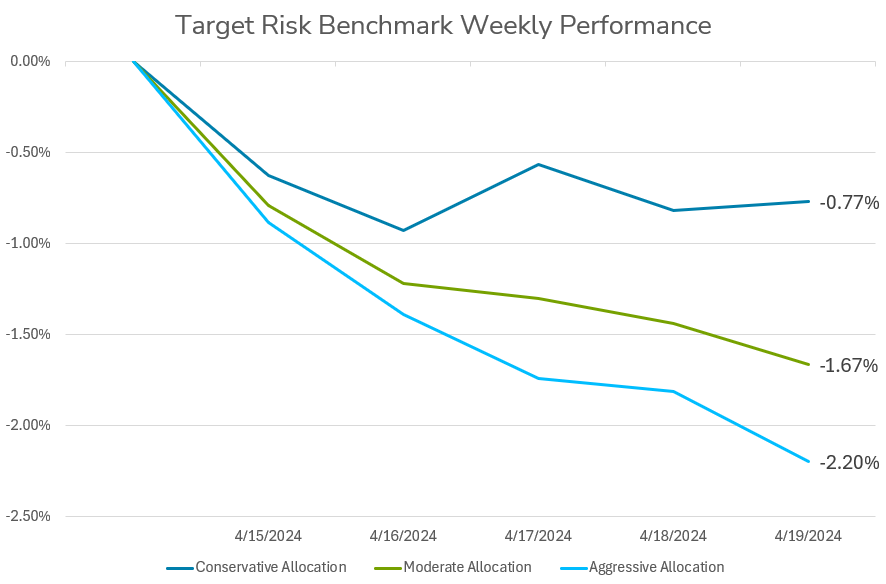

Investors in balanced multi-asset portfolios experienced a second consecutive week of losses driven by declines in both stocks and bonds, as shown by the target risk benchmarks below. The aggressive risk benchmark has a roughly 90% allocation to the Russell 3000 and MSCI All Country World Index Ex USA, with limited exposure to the US Aggregate Bond Index. Meanwhile, the moderate risk benchmark is a 60/40 split of global equities and bonds, while the conservative risk benchmark has a roughly 90% allocation to US bonds. Geopolitical concerns regarding the conflict between Israel and Iran weighed on risk assets to start the week. Then in the middle of the week several US Federal Reserve officials made hawkish comments regarding the path of interest rates, indicating that the Fed may not be able to lower interest rates in an environment of continued above-target inflation coupled with ongoing momentum in the economy. This sent the yield on the US 10 Year Treasury note well above 4.5%, though it retraced slightly to end the week at 4.62%. Equities came under pressure as well, as several of the large technology companies sold off as quarterly earnings announcements come into focus. Nvidia Corp and Super Micro Computer Inc. both sold off substantially on Friday as chipmakers reported weaker demand than expected. Netflix Inc also tumbled to end the week due to a weak forecast for revenue growth moving forward. The conservative risk benchmark recovered its earlier fall slightly to end the week down -0.77%, while the moderate and aggressive risk benchmarks continued to drop throughout the week, ending with losses of -1.67% and -2.2% respectively.

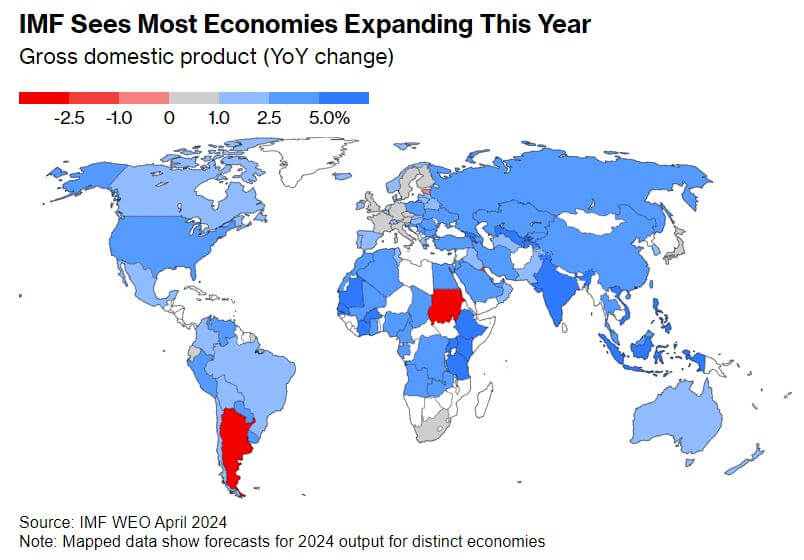

The International Monetary Fund (IMF) has revised its global economic growth forecast slightly upward, now expecting a 3.2% expansion in 2024, citing strength in the US and select emerging markets. However, the outlook remains cautious due to persistent inflation and geopolitical risks. While the IMF's projection aligns closely with Bloomberg Economics' estimate, it warns of challenges such as high borrowing costs and the withdrawal of fiscal support, which are dampening short-term growth. Moreover, long-term prospects are subdued due to low productivity and global trade tensions. While the world economy has avoided the worst stagflation outcomes post-pandemic, its potential for growth in the coming years is hindered. The IMF also issued a warning about financial stability risks, particularly regarding a potential resurgence of consumer-price growth. Tobias Adrian, responsible for capital markets at the IMF, highlighted the threat posed by high inflation and investors' expectations of monetary policy easing. Furthermore, the IMF expressed concern about the under-performance of low-income countries, attributing it to factors such as the stronger US dollar and elevated food, fuel, and fertilizer costs. IMF Chief Economist Pierre-Olivier Gourinchas noted that while the US economy has rebounded strongly, many low-income developing countries still struggle with pandemic-related challenges. Geopolitical risks, especially conflicts in Ukraine and the Middle East, pose additional threats to global economic stability. Regarding specific economies, the IMF adjusted its growth forecasts, with the US seeing an upward revision but the Euro area facing downward pressure due to tighter monetary policy and increased energy costs. China's growth outlook remained steady, with concerns about its real estate sector and export practices. The IMF also highlighted fiscal policy concerns in the US, stating that while the nation's economic performance is impressive, its budget policy poses risks to long-term fiscal sustainability and global financial stability.

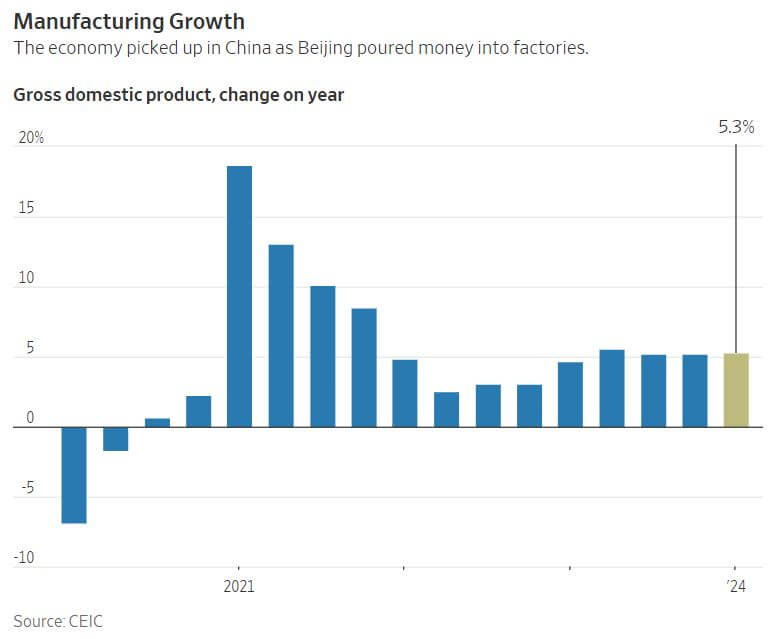

The first quarter of 2024 witnessed a notable acceleration in China's economy, attributed largely to Beijing's concerted effort to stimulate growth by injecting funds into manufacturing sectors, yielding discernible results. The National Bureau of Statistics of China reported a 5.3% year-over-year growth rate for the economy during this period, surpassing the 5.2% growth registered in the preceding quarter. This upturn was propelled by an uptick in industrial production and increased investment in manufacturing facilities, marking a strategic shift to bolster these sectors amidst sluggish domestic consumption and persistent challenges in the real estate market. However, concerns persist regarding the sustainability and inclusivity of this recovery. Notably, there is apprehension regarding the concentration of growth in manufacturing, potentially exacerbating trade tensions with Western nations and other emerging economies. Critics argue that the emphasis on manufacturing and exports may lead to a disproportionate reliance on external demand and could neglect the needs of Chinese households. The decline in property investment and tepid retail sales growth underscore lingering weaknesses in consumer sentiment, compounded by anxieties over employment stability. Despite the positive momentum in industrial production, there are signs of strain, such as diminishing demand relative to supply and declining industrial capacity utilization rates. This underscores the challenges of sustaining growth without addressing underlying demand-side constraints. While Beijing has implemented measures to stimulate household spending, including interest rate cuts and incentive programs, economists advocate for more comprehensive support to mitigate deflationary pressures and rebalance the economy towards consumption-driven growth.