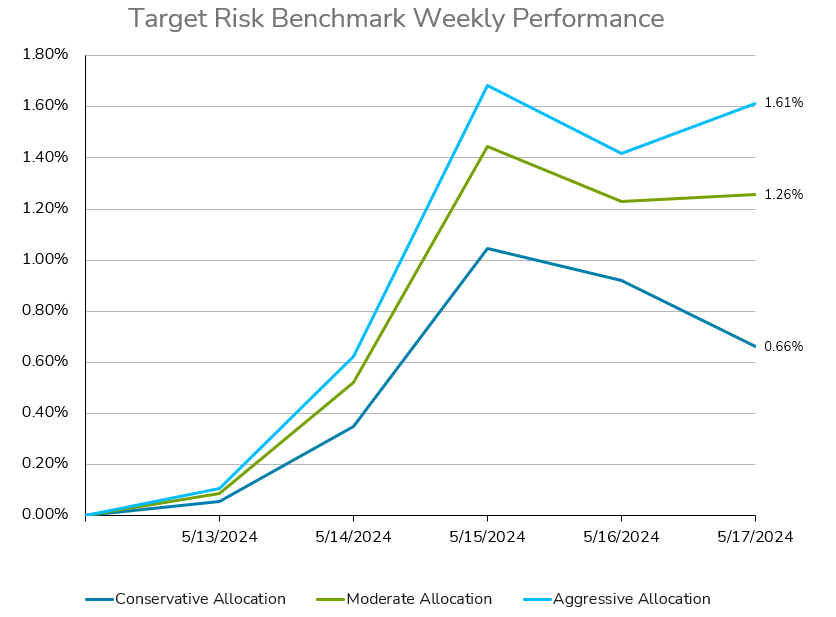

Investors in multi-asset balanced portfolios enjoyed another week of substantial gains, as shown by the performance of the risk tolerance benchmarks. The aggressive risk benchmark has a roughly 90% allocation to the Russell 3000 and MSCI All Country World Index Ex USA, with limited exposure to the US Aggregate Bond Index. The moderate risk benchmark is a 60/40 split of global equities and bonds, while the conservative risk benchmark has a roughly 90% allocation to US bonds. Stocks continued their upward trajectory for a fourth consecutive week, with the Dow Jones Industrial Average surpassing the 40,000 mark for the first time. This bullish trend was driven by favorable inflation reports that bolstered hopes for Federal Reserve rate cuts, along with strong corporate earnings. The S&P 500 experienced its longest weekly winning streak since February, despite some cooling in momentum over the past two days. All risk tolerances benefited from the relatively benign inflation report on Wednesday, which boosted both stocks and bonds. However, towards the end of the week, Treasury yields increased, signaling cautious optimism about the strength of the economy. That resulted in the conservative risk tolerance benchmark giving up some of its gain for the week, finishing up 0.66%. In contrast, the moderate and aggressive risk tolerance benchmarks rebounded on Friday, finishing with gains of 1.26% and 1.61% for the week, respectively.

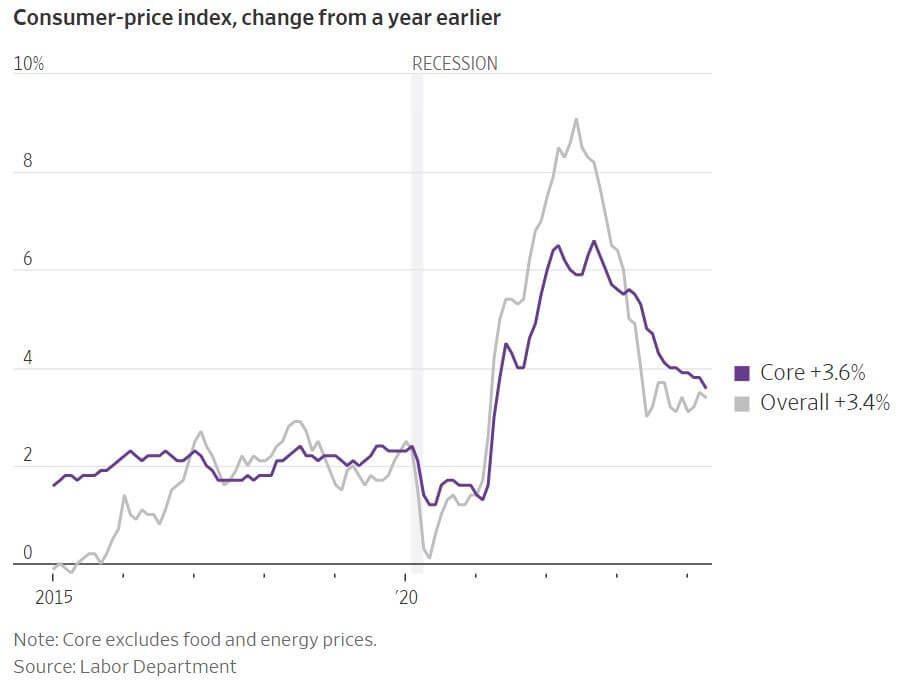

In April, U.S. inflation showed a slight decrease for the first time in six months, providing some respite to investors and the Federal Reserve amidst ongoing price pressures earlier in the year. The consumer-price index (CPI) rose 3.4% annually, with core prices (excluding food and energy) increasing 3.6%, the smallest rise since April 2021. The core CPI increased 0.3% month-over-month. Economists view the core measure as a more accurate indicator of underlying inflation trends. Key contributors to the CPI increase included shelter and gasoline, which accounted for over 70% of the rise. Service-related costs, such as car insurance and medical care, also contributed significantly, with apparel prices experiencing their largest jump since June 2020. Shelter prices, particularly owners’ equivalent rent, continued to rise, highlighting robust housing costs as a persistent driver of inflation. The cooling of core goods prices, excluding food and energy, provided some relief, driven by a slight decline in motor vehicle prices. The data, which came in line with forecasts, alleviated concerns about entrenched inflation following three months of higher-than-expected readings. This development offers a glimmer of hope for Federal Reserve officials considering rate cuts later this year. Market reactions were positive on Wednesday, with Treasury yields falling, the S&P 500 opening higher, and the dollar weakening. Despite the deceleration in core inflation, the broader economic landscape remains complex. A recent report showed producer prices rose more than expected in April, though key categories affecting the personal consumption expenditures (PCE) price index, which the Fed closely monitors, were more subdued. A separate report revealed real earnings on an annual basis rose at the slowest pace in nearly a year, showing continuing cooling in the labor market. Another report indicated retail sales stagnated in April, suggesting high borrowing costs and increasing debt are leading consumers to be more cautious. Fed Chair Jerome Powell emphasized the need for patience, indicating that restrictive monetary policy must be given time to impact the economy. Some policymakers remain skeptical about cutting rates this year, though traders have increased the likelihood of a September rate cut to about 60%.

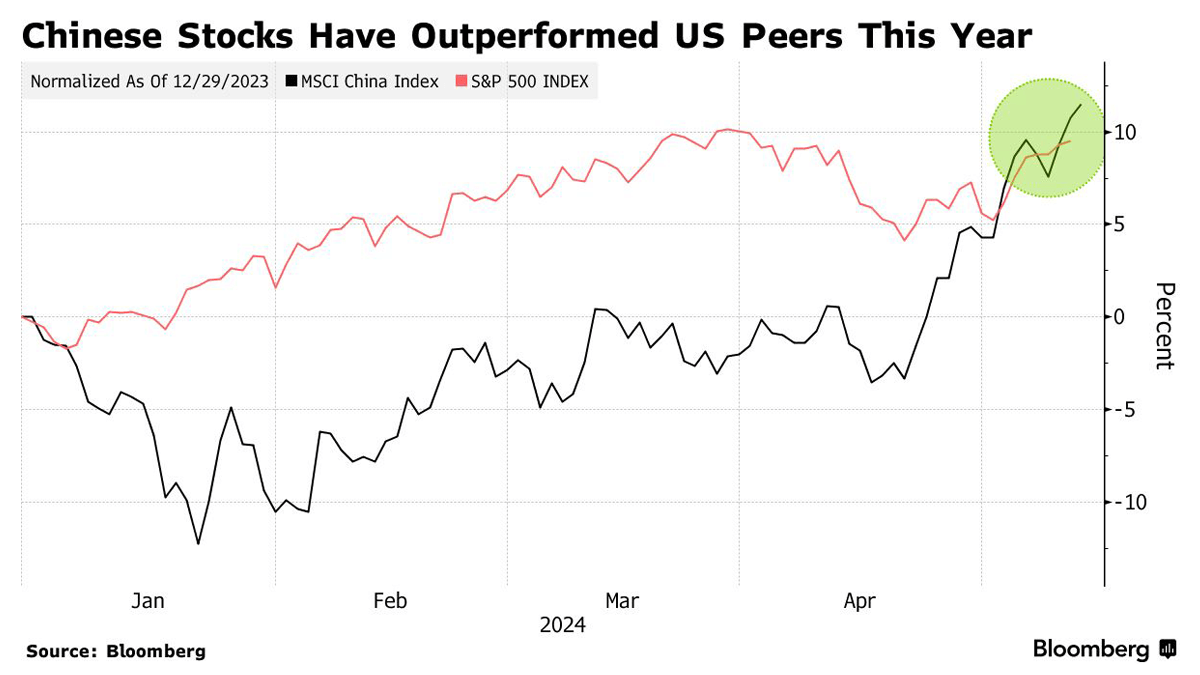

Chinese stocks have shown signs of recovery with the MSCI China Index gaining 27% since its January low. This uptick, driven largely by attractive valuations and rotational investment strategies, has yet to be substantiated by robust earnings growth. Money managers, including those from Lombard Odier, Pictet Asset Management, and Fidelity International, remain cautious, emphasizing the need for companies to demonstrate consistent profit gains before committing to significant reinvestments. Despite the rally, which has brought back approximately $2.5 trillion of market value, there is skepticism about the sustainability of this rebound. The historical pattern of bear market rallies in China adds to the hesitation. John Woods, Chief Investment Officer for Asia at Lombard Odier, stresses the importance of focusing on earnings and fundamentals rather than attempting to time the market. The recent surge has been partly fueled by a rotation from other high-performing markets such as the US, Japan, and India, to Chinese stocks, which are currently trading at historically low valuations. April marked the third consecutive month of net buying of onshore stocks by overseas investors via Hong Kong trading links, a trend not seen in a year. The MSCI China Index's valuation stands at 10 times forward earnings, which is below its five-year average. Consensus earnings growth for Chinese stocks is pegged at around 10%, but John Lin from AllianceBernstein argues this is overly optimistic, noting the need for stronger corporate performance. The ongoing earnings season has revealed a nearly 30% decline in net profit among the index's constituents, heightening concerns. The rally is also supported by anticipated policy measures from Beijing, particularly in the real estate sector.

Xi Jinping's government launched its most decisive effort yet last week to rescue China's struggling property market by relaxing mortgage rules and urging local governments to purchase unsold homes. The package includes lower down-payment requirements for homebuyers and 300 billion yuan ($42 billion) from the central bank to assist government-backed firms in buying excess inventory from developers, which will then be converted into affordable housing. While this move was welcomed by equity investors, with developer shares rising nearly 10%, skepticism remains about its effectiveness in resolving the property crisis. The central bank’s funding is a fraction of the estimated 1 to 5 trillion yuan needed to address the supply-demand imbalance in housing, and many buyers are hesitant, waiting for further price drops. Despite multiple measures introduced over the past year, housing prices have continued to decline, with April recording the steepest monthly drop in a decade. Lowering mortgage rates has yet to significantly boost demand, with over 40% of cities reducing or scrapping mortgage rate floors by March. Ultimately, the effectiveness of these measures will depend on consumer confidence. Without robust execution and a shift in household expectations, the policy may not achieve a substantial structural turnaround in the property market.