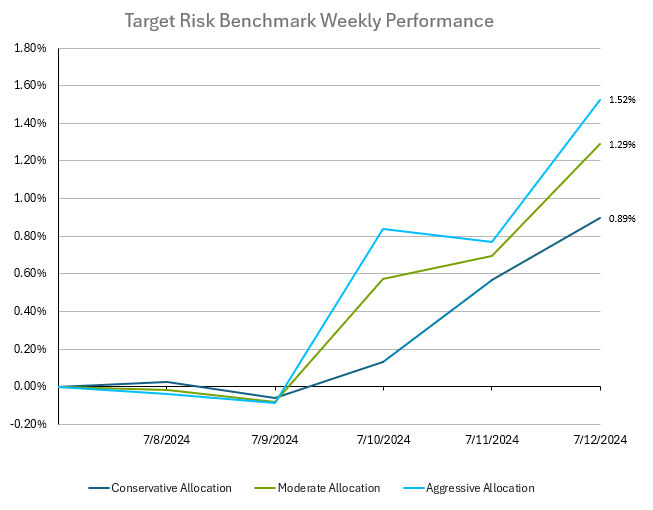

Investors in balanced multi-asset class portfolios enjoyed healthy gains across all risk tolerances last week. The aggressive risk benchmark below has a roughly 90% allocation to global equities, with a small allocation to bonds. Meanwhile, the moderate risk benchmark is a 60/40 split of global equities and bonds, while the conservative risk benchmark has a roughly 90% allocation to US bonds. The major catalyst for markets this week was the June consumer price index (CPI) data, which came in below expectations. Markets shrugged off weak consumer sentiment data and producer price index (PPI) data that came in above estimates, as another month of soft inflation data has led many analysts to believe that the Fed in on track to cuts rates, possibly as soon as September. Treasuries rallied, with US 10-year yields declining to 4.18% to end the week. The Bloomberg US Aggregate Bond Index ended the week with a strong gain of 0.83%. Smaller firms' rebound was significant, with the Russell 2000 viewed as an indicator of interest-rate easing and economic conditions. The Russell 2000 index had its best week since November. Market analysts are debating whether the recent market rotation indicates a trend reversal or a temporary shift. While US markets as measured by the Russell 3000 Index had a substantial gain of 1.38% for the week, international equities had an even stronger period, with the MSCI ACWI ex USA IMI Index gaining a full 2.01%. Future economic data and earnings reports are expected to provide further clarity on market direction.

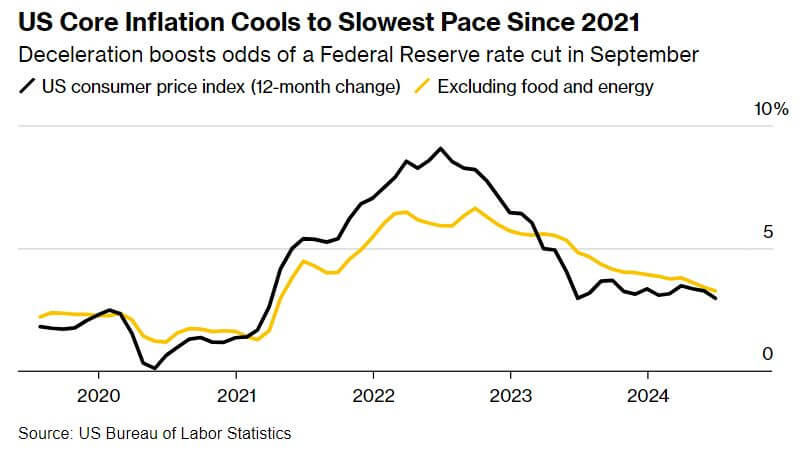

In June, U.S. inflation notably decreased, continuing a recent trend that could prompt the Federal Reserve to cut interest rates. The consumer-price index, which tracks overall economic costs, fell slightly from May, bringing the year-over-year inflation rate down to 3%, the lowest since June 2023. Core prices, excluding volatile food and energy items and better reflecting underlying inflation, increased by just 0.1% from May—the smallest rise since January 2021. The annual core inflation rate also dropped to 3.3%, the lowest since 2021. This broad cooling of prices in the second quarter surpassed economists' expectations, contrasting with unexpectedly brisk inflation in the first quarter. Continued mild inflation could support a potential interest-rate cut in September, especially if the labor market shows signs of cooling, which could reduce ongoing inflation or signal economic weakness. Investors currently do not expect a rate cut at the Fed's next meeting on July 30-31, as officials have not publicly rallied consensus for such a move. Instead, the focus will be on whether the groundwork for a September cut is laid. Thursday’s inflation report and two additional readings on June prices are critical, as they are the last data available before the July meeting. The report was reassuring for policymakers, showing a slowdown in housing costs after a significant post-pandemic increase. This aligns with expectations, as rents for new housing units have been cooling for 1.5 years, confirming that official inflation measures are now capturing these developments. Recent economic data indicate a cooling economy, with household consumption, construction spending, and service sector activity all below expectations. This has lowered estimates for economic growth in the second quarter. Despite this, employers have added over 200,000 jobs monthly on average this year, though the unemployment rate rose to 4.1% in June from 3.7% in December, suggesting a growing workforce and easing labor demand. Federal Reserve Chair Jerome Powell recently indicated that further labor market cooling might be undesirable, noting that the labor market is not currently a source of broad inflationary pressures. Many economists remain cautiously optimistic about inflation returning to the Fed's 2% target, despite a potentially slow and uneven path.

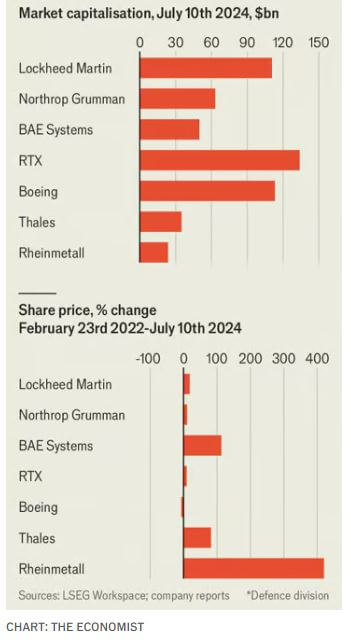

The arms industry operates uniquely, insulated from macroeconomic trends and consumer preferences, driven primarily by the perceived military threats faced by its government customers. Recent conflicts in Ukraine, Gaza, potential tensions between Israel and Lebanon, and China's interest in Taiwan have heightened threat perceptions, influencing NATO's defense spending. In 2023, NATO's 32 members spent $1.3 trillion on defense, a record high since the Soviet Union's fall, with the U.S. alone budgeting $842 billion. NATO's traditionally frugal European members are reversing decades of underinvestment in military equipment, with 18 members expected to meet the 2% of GDP defense spending target this year, up from just three in 2014. Of NATO's total defense budget, $360 billion was allocated to weapons systems and major equipment, double the share from ten years ago, and this trend is expected to continue. This surge in defense spending benefits American prime defense contractors like Lockheed Martin, RTX, and Northrop Grumman. However, despite a substantial budget for procurement and R&D, their market values have stagnated since Russia's invasion of Ukraine. In contrast, European firms like Thales, BAE Systems, and Rheinmetall have seen significant share price increases. American defense contractors face capacity constraints due to years of reduced production post-Cold War and a shift in priorities post-9/11 towards counterterrorism and maritime defense against China. Restoring this capacity will take years and depends on sustained demand. Meanwhile, European defense spending is increasing more predictably. Additionally, the U.S. Department of Defense (DoD) is shifting procurement strategies, moving from cost-plus to fixed-price contracts, which place more financial risk on contractors. This change has led to losses for firms like Northrop Grumman and Boeing. The DoD is also emphasizing agile, smart systems over traditional large-scale platforms, attracting competition from newer, non-traditional defense firms like Anduril and Palantir, which are winning significant contracts. Despite challenges, legacy programs and rising foreign military sales continue to support American prime contractors. Future increases in U.S. defense spending remain possible, especially with political changes or supplementary appropriations. Although the prime contractors must adapt to new procurement dynamics and competition, they remain influential players in the defense sector.