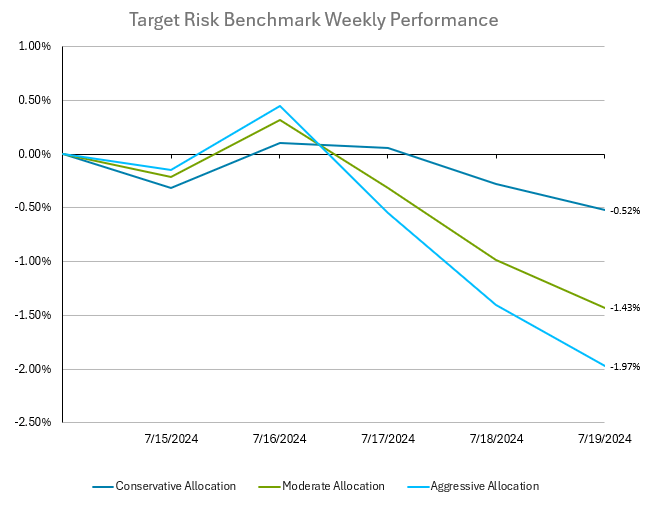

Stocks ended the week on a downtrend as major technology companies prepare to report earnings at a critical juncture for Wall Street. The S&P 500 experienced its worst week since April, driven by a rotation where investors shifted from this year’s high performers to laggards such as value stocks and small caps. This move anticipated a broader market rally with expected Federal Reserve rate cuts in 2024. Tech stocks, particularly the “Magnificent Seven” mega-caps, fell 5% on Friday, with semiconductor stocks like Nvidia and Intel dropping nearly 9%. This coming week will be pivotal, with key earnings reports from tech giants and economic data releases, including the Fed’s preferred price gauge. Analysts suggest strong tech earnings and easing inflation could reverse recent market weaknesses. Treasury yields rose slightly, and economic data supported expectations for easier monetary policy. Lower rates could benefit small caps, though a significant market shift is not yet certain. Tesla and Alphabet will report earnings first, followed by Microsoft, Meta, Amazon, and Apple in the subsequent week. Goldman Sachs strategists anticipate a potential market correction rather than a bear market, influenced by weaker growth data, dovish central bank expectations, and rising policy uncertainty ahead of the US elections. Despite recent market moves, US equity funds saw significant inflows, indicating strong investor confidence in forthcoming Fed rate cuts and election outcomes. International stocks endured a tough week as well, with the MSCI ACWI ex-USA IMI Index finishing the week with a loss of -2.91%. In this environment, multi-asset class balanced portfolios had a week of losses through a choppy week of trading, giving up the gains from the prior week following a benign CPI data release. The aggressive risk benchmark below has a roughly 90% allocation to global equities, with a small allocation to bonds. The moderate risk benchmark is a 60/40 split of global equities and bonds, while the conservative risk benchmark has a roughly 90% allocation to US bonds. The aggressive target risk benchmark finished the week with a loss of nearly 2%, while the moderate target risk benchmark was not far behind with a loss of -1.43%. Bonds held up much better than equities for the week, limiting losses for the conservative target risk benchmark to -0.52%.

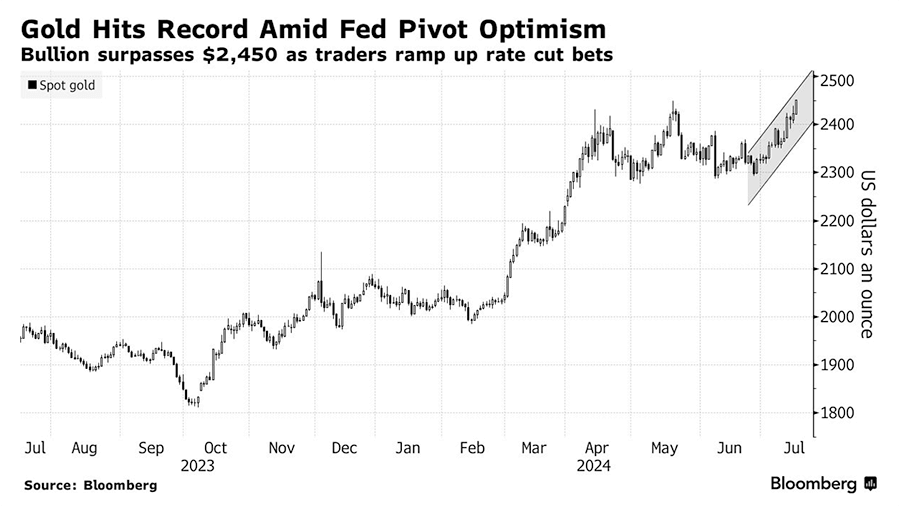

Gold prices surged to an all-time high of $2,469.66 an ounce, surpassing the previous peak set in May, driven by growing expectations of Federal Reserve rate cuts and increased speculation of a second Donald Trump presidency. This rally is attributed to signals of slowing inflation in the US, prompting speculation that the central bank may soon lower interest rates. Typically, high interest rates negatively impact gold, which does not yield interest. However, gold has risen nearly 20% this year, buoyed by significant central bank purchases, strong consumer demand in China, and heightened interest in haven assets due to geopolitical tensions. The recent increase in exchange traded fund holdings has also contributed to the upward momentum. Ewa Manthey, a commodities strategist at ING Bank NV, noted that optimism about US interest rate cuts, supported by economic data, is bolstering gold. She highlighted that gold is likely to maintain its positive momentum amid the current geopolitical and macroeconomic environment, with central bank demand expected to grow. Fed Chair Jerome Powell indicated that recent data has increased confidence that inflation is moving towards the central bank's 2% target, leading traders to anticipate two quarter-point rate cuts this year. Goldman Sachs has suggested that conditions are favorable for easing, potentially as soon as July. The upward trend in gold was anticipated by some analysts, with consultancy Metals Focus predicting a new record this year and Citigroup forecasting gold prices between $2,700 and $3,000 an ounce by 2025. Additionally, speculation around Trump's potential return to the White House, following a failed assassination attempt and the dismissal of a criminal case against him, is influencing market sentiment. David Higgins of Merrion Gold suggested that a Trump presidency might drive retail customers to buy gold due to perceived instability.

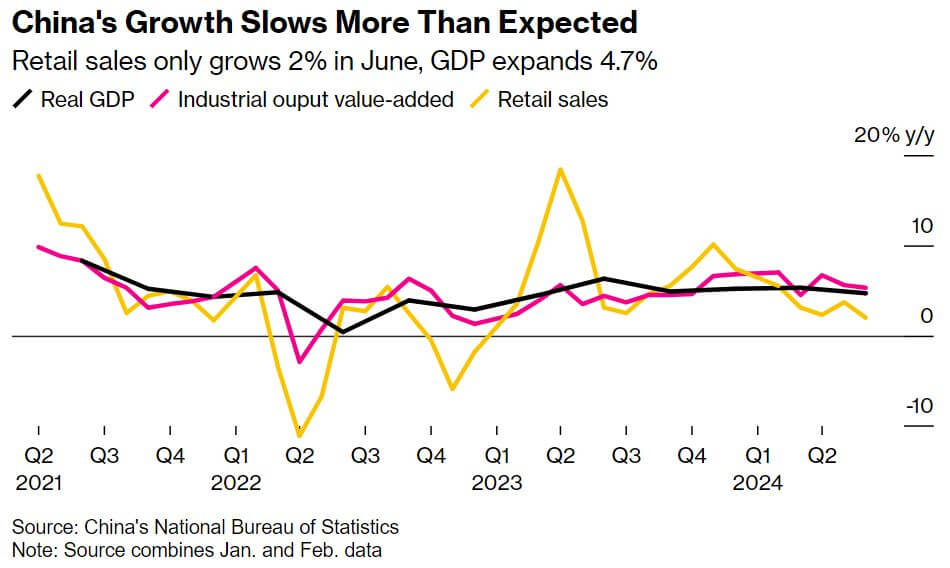

Last week, Chinese leader Xi Jinping and top Communist Party officials convened in Beijing for the Third Plenum meeting to address the nation's faltering economy. China's economic growth slowed to a five-quarter low of 4.7% in Q2 as weak consumer spending countered an export surge, below most forecasts. Retail sales saw their slowest growth since December 2022, highlighting ineffective government efforts to boost consumer confidence. President Xi’s focus on manufacturing and high-tech sectors supported industrial production, but geopolitical risks persist, notably with potential tariff hikes from a re-elected Donald Trump. Following the disappointing economic data, the People's Bank of China maintained its benchmark rate amid concerns about capital flight and bank profits. China's persistent housing crisis and deflationary trends further dampen economic prospects. Government subsidy programs have had mixed results, and household consumption remains weak amid high youth unemployment and salary cuts. The four-day Third Plenum meeting culminated in a communiqué that underscored Xi's commitment to state-led development, despite growing concerns among citizens and foreign investors. The communiqué candidly acknowledged economic challenges, highlighting risks in the property sector, local-government debt, and small and midsize financial institutions. However, it did not propose substantial changes, reaffirming Xi's focus on economic security and technological dominance. This approach has been criticized for exacerbating economic imbalances. Steve Tsang of the SOAS China Institute noted that the communiqué reaffirmed Xi's direction for China, despite serious economic challenges, emphasizing Communist Party control to ensure political stability but offering little to restore economic vitality. The document signaled an intention to strengthen the state's central role in economic development, rather than increasing market and consumer influence, as some economists have advocated. China's economy faces multiple challenges: a housing market crisis, local government debt, reduced consumer spending, and escalating trade tensions, compounded by a rapidly aging population. Solutions are complex, with deep structural overhauls needed, particularly in local government funding. However, the lack of any major policy changes or fiscal support for the economy following the Third Plenum suggests that these problems will grind on, lowering the appeal of Chinese financial assets for investors.