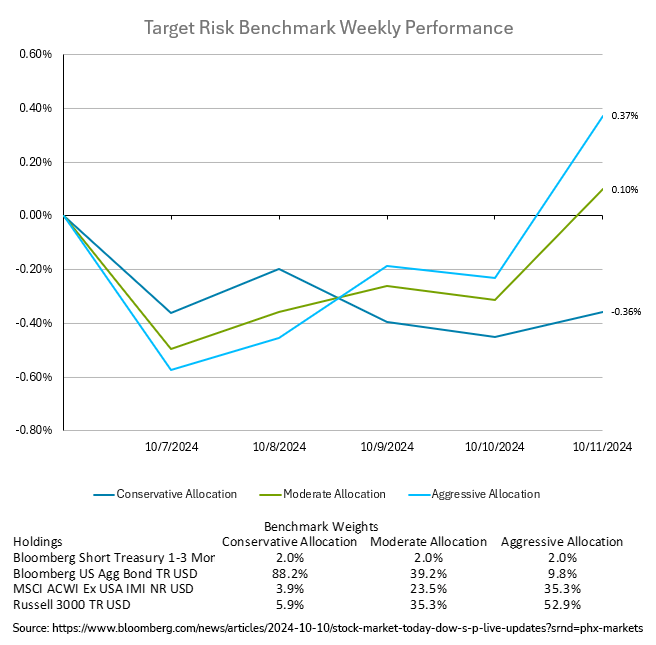

Wall Street began the earnings season with stocks hitting record highs, driven by big banks' solid performance. The S&P 500 reached 5,800, marking its 45th record high in 2024 and continuing a five-week winning streak. Concerns that Federal Reserve rate cuts might hurt bank profits were dispelled as JPMorgan Chase posted a surprise increase in net interest income (NII), while Wells Fargo saw a smaller-than-expected decline. Major bank stocks surged, pushing the KBW Bank Index to its highest since April 2022. However, the Bloomberg US Aggregate Bond Index fell -0.46% for the week as economic data came in stronger than expected. Tesla fell 8.8% after an underwhelming robotaxi reveal, while Uber and Lyft shares jumped over 9.5%. Oil prices settled below $76 per barrel despite tensions in the Middle East. Investors are optimistic about the earnings season, particularly for big banks, as economic activity is expected to drive revenues. Analysts expect S&P 500 companies to surpass lowered earnings expectations, with forecasts for 4.2% net income growth for the third quarter. In the broader markets, the dollar remained steady, Bitcoin surged 5.5%, and gold prices rose. The risk-on shift in markets to end the week benefited aggressive multi-asset portfolios at the expense of conservative risk tolerances, as seen below. The aggressive target risk benchmark gained 0.37% for the week, while the gains in equities were essentially cancelled out by the losses in fixed income in the moderate target risk benchmark. The conservative target risk benchmark had a loss of -0.36% for the week.

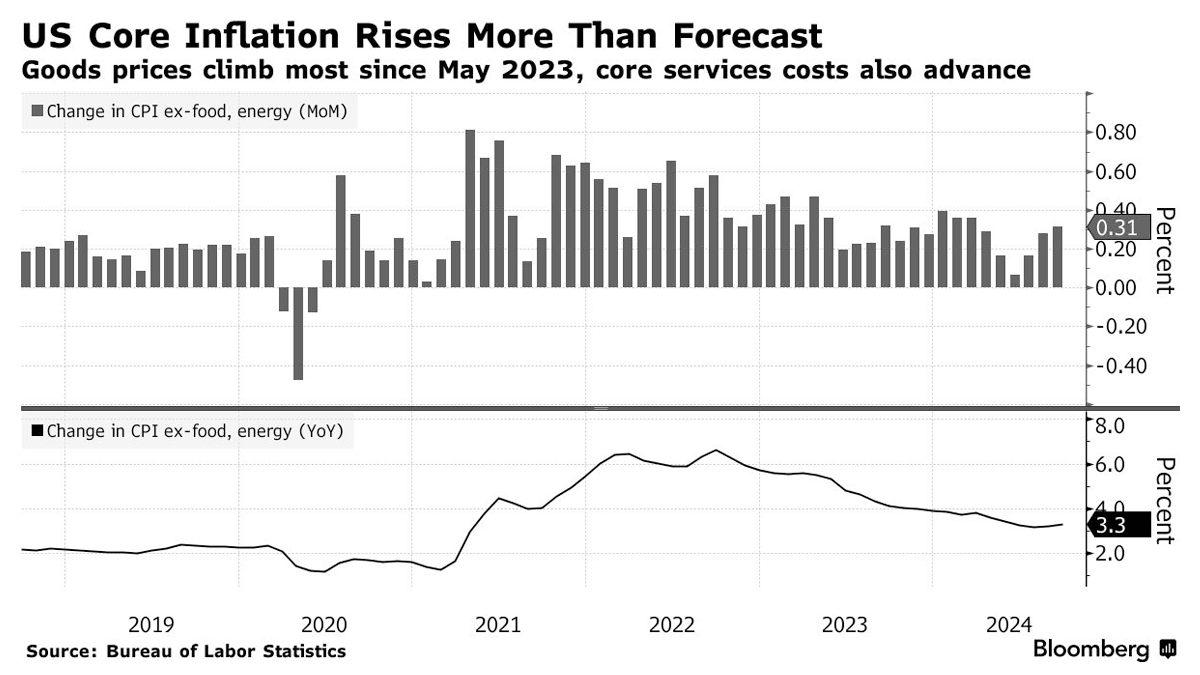

U.S. inflation reached a three-year low in September, with the Consumer Price Index (CPI) rising by 2.4% year-over-year, compared to 2.5% in August, according to the Labor Department. However, this increase exceeded economists' expectations of 2.3%. Core inflation, excluding food and energy, also decreased at a slower rate than anticipated, climbing 3.3% over the previous 12 months. Core CPI rose 0.3% for the month, matching August’s rate. This gradual deceleration in inflation highlights the ongoing challenges faced by policymakers, as price growth remains uneven across sectors. While energy prices, particularly gasoline, saw notable declines, prices for essentials like housing, food, and car insurance rose sharply. Bond investors scaled back expectations for a November interest-rate cut following comments by Atlanta Federal Reserve President Raphael Bostic. Earlier in the day, traders had priced in over an 80% chance of a quarter-point reduction after an uptick in jobless claims. However, Bostic's suggestion of potentially pausing cuts led to a reassessment, with the probability of a November cut dropping to about 75%. For 2024, traders are still anticipating around 43 basis points of total rate cuts, slightly higher than before the latest economic data release. Bostic’s remarks also affected the Treasury market, particularly short-term yields, which rose as two-year Treasury yields edged close to 4%. Despite the inflationary pressures, Federal Reserve Bank of Chicago President Austan Goolsbee downplayed inflation concerns, emphasizing labor market conditions as the key driver for future Fed decisions. Fed officials appear cautious, with some advocating for a more gradual pace of rate cuts following last month’s half-point reduction. This uncertainty creates opportunities for investors to capitalize on higher yields, especially in short-term bonds.

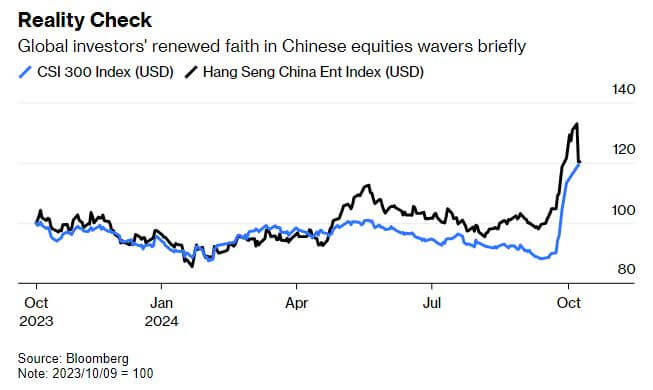

China’s onshore CSI 300 stock index surged 10% after the Golden Week holiday, fueled by anticipation of a large fiscal stimulus package from the National Development and Reform Commission (NDRC). However, investors were disappointed when the agency announced only 200 billion yuan in spending, far below expectations of a 3 trillion yuan package. The initial market rally subsided, with the CSI 300 retaining a 6% gain, while offshore investors experienced a selloff exceeding 10% in Hong Kong’s Hang Seng China Enterprises Index. The sharp shortfall in the announced stimulus versus expectations tempered market enthusiasm, but some analysts believe China’s rally may still have room to run. Officials seem cautious about fueling excessive market exuberance, mindful of the 2015 boom and bust, when the CSI 300 rose 60% before crashing. By moderating expectations, authorities aim to avoid repeating past mistakes that damaged market confidence and led to emergency interventions. While investors showed impatience with the NDRC's limited fiscal response, attention has shifted to the Ministry of Finance, which is expected to deliver more substantial stimulus, potentially around 2-3 trillion yuan. A further disappointment could harm market confidence, but a larger fiscal stimulus could give equities a further leg up. Despite the recent surge, concerns over corporate governance and government interference persist, deterring some international investors. However, sectors such as Macau casinos, internet platforms, energy, and education are seen as safer bets, offering higher barriers to entry and some protection from government interventions. Still, China’s unpredictable market messaging continues to challenge investors’ confidence, casting doubt over the long-term sustainability of the rally.