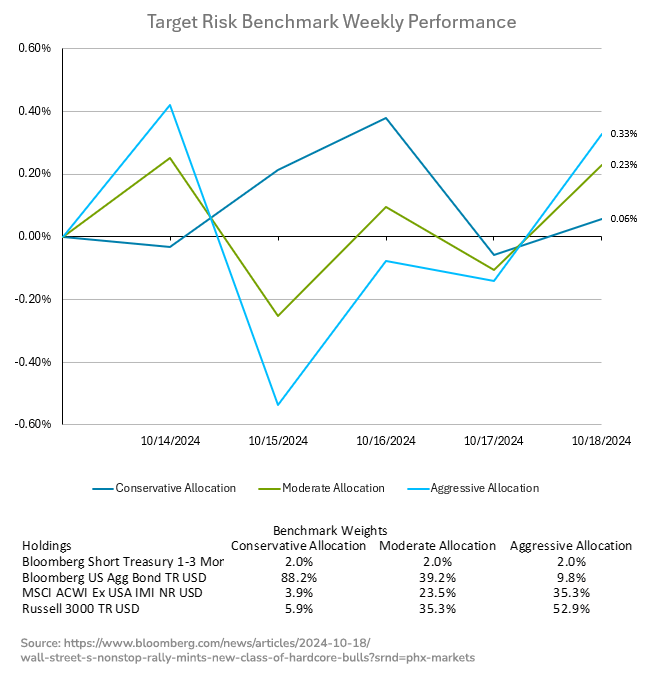

Despite market concerns over stretched valuations, narrowing bond spreads, and record-high gold prices, some investors remain bullish. While many are hedging gains, a growing number argue that the economy still supports riskier assets, driven by resilient corporate earnings and consumer strength. The Atlanta Fed revised its GDPNow forecast to 3.4% for Q3, further supporting the narrative of economic strength. Though S&P 500 valuations remain elevated at 24 times earnings, the economy has defied recession fears, with positive bank earnings and strong labor data driving optimism. Despite volatility, retail and institutional investors continue buying market dips, bolstering equities. Global central banks are easing policies, fueling bullish sentiment. Traders poured $3.2 billion into risk-on ETFs, the fastest pace since August, reflecting growing confidence. The S&P 500 rose nearly 1% for its sixth consecutive weekly gain, marking its longest streak since December, while oil posted its first weekly decline of the month. Ten-year Treasury yields steadied following a recent climb, and investment-grade corporate bonds had their best rally in weeks. Gains in domestic equities were partially offset by losses in international equities last week, while the Bloomberg US Aggregate bond index was near flat. That environment delivered small gains to multi asset class investors across all risk tolerances, as shown in by the target risk benchmarks below. The aggressive target risk benchmark had a small gain of 0.33%, while the moderate target risk benchmark was not far behind with a gain of 0.23%. The conservative target risk benchmark was essentially flat for the week with a gain of 0.06%.

The European Central Bank (ECB) cut interest rates for the third time in 2024, reducing the key deposit rate by 25 basis points to 3.25%, as inflation drops faster than expected. While policymakers signaled that inflation may return to target levels by 2025, they provided no clear timeline for further rate adjustments. The ECB emphasized that monetary policy will remain "restrictive" as long as needed to ensure price stability. ECB President Christine Lagarde highlighted the challenges facing the eurozone, including weaker growth prospects, falling private-sector activity, and a softening labor market. Despite these risks, Lagarde downplayed the likelihood of a recession, maintaining hope for a "soft landing." However, geopolitical uncertainties—such as the conflict in the Middle East, potential trade frictions with China, and uncertainty around U.S. tariffs—pose additional threats to economic recovery. Recent data shows inflation easing to 1.7% in September, though persistent pressure in the services sector suggests the battle against inflation is not yet fully won. Meanwhile, Mediterranean economies like Spain and Greece have shown resilience, though Germany, the region’s economic heavyweight, continues to struggle amid subdued global demand. Market expectations point to further rate cuts at each ECB meeting through March 2025, with rates potentially stabilizing around 2% by the end of 2025— aligning with the estimated "neutral" policy range. Policymakers remain cautious, acknowledging downside risks to growth, with some suggesting that the pace of monetary easing may accelerate if economic conditions worsen.

While inflation has been drifting downward towards central bank targets, could a jump in oil prices put upward pressure on inflation once again? Since Hamas attacked Israel last year, oil markets have feared that escalating tensions could lead to a regional conflict involving Iran, a major oil producer. Until recently, both Israel and Iran seemed to avoid direct confrontation, keeping oil prices relatively stable. However, Iran’s missile attacks on Israel on October 1st have raised concerns, leading to a 10% increase in crude prices to $78 a barrel. Analysts now speculate how Israel’s potential retaliation could impact oil markets. If Israel limits its strikes to military targets, oil prices might stabilize. However, attacks on Iran’s oil infrastructure—such as the Abadan refinery or Kharg Island’s oil terminals—could disrupt global supply, though OPEC+ has sufficient spare capacity to compensate for lost Iranian output. This could mitigate extreme price increases, unlike during Russia’s invasion of Ukraine in 2022. Production from non-OPEC nations, like the U.S. and Brazil, is also rising, further softening potential shocks. Diplomatic risks loom if Israel strikes Iran's oil assets. The U.S. could object due to its domestic economic concerns, and China, Iran's main oil customer, might react unfavorably. While oil markets could briefly spike by $5-10 per barrel, analysts do not expect prices to sustain a steep rise unless the conflict escalates dramatically. More severe scenarios, such as Iran closing the Hormuz Strait—through which 30% of global seaborne oil passes—would cause significant disruption but hurt Iran’s own economy. In such a case, the U.S. and China would likely intervene to reopen the strait. Overall, though oil markets are jittery, analysts predict that only a major, prolonged disruption would push prices toward the $130 per barrel peak last seen in 2022. Otherwise, current global supply and sluggish demand should keep prices from climbing too high.