The 10-year Treasury bond yield rose by 0.25 percentage points to 4.398% this week, marking the largest weekly increase since October 2023. This reversed a trend of steady declines since the presidential election, with the rise in yields reflecting investor concerns about the path of interest rates. The bearish bond market weighed on equities, including large-cap technology stocks like Alphabet, Amazon and Nvidia, which ended slightly lower on Friday. Additionally, fears of inflation impacting spending by lower-income consumers pressured consumer-goods stocks such as Nike and Coca-Cola. US equities ended mixed on Friday, with the S&P 500 closing flat, recording its weakest weekly performance in a month. The Nasdaq 100 rose 0.8%, driven by a surge in Broadcom, which forecasted strong demand for its AI chips, boosting semiconductor shares. However, the broader S&P 500 showed signs of fatigue, with more constituents lagging than gaining for a record-setting 10 consecutive sessions. Small-cap stocks, which had previously outperformed following Donald Trump’s election, have now erased those gains relative to the S&P 500.

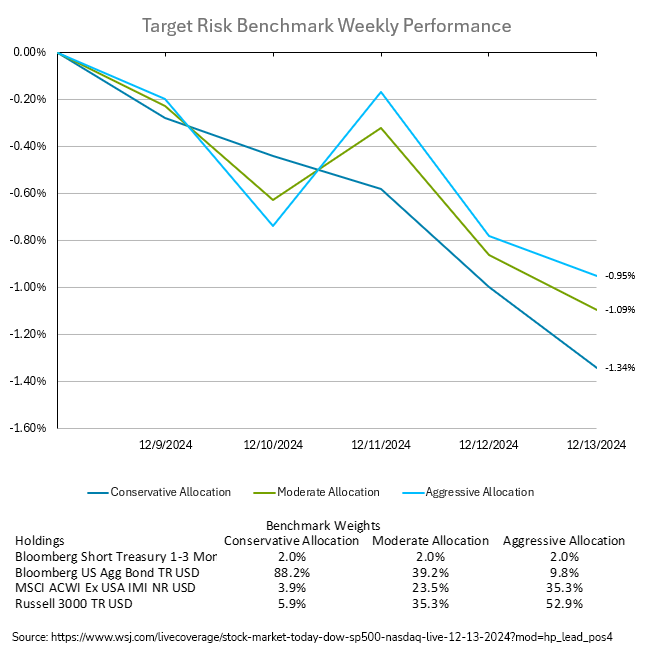

The losses for the week were broad based across all asset classes, impacting investors regardless of risk tolerance. The large rise in bond yields for the week hit conservative investors the hardest, with the conservative target risk benchmark falling 1.34%. However, both domestic and international equities struggled for the period as well, meaning moderate and aggressive investors did not fare much better. The moderate target risk benchmark fell 1.09% for the week, while the aggressive target risk benchmark held up slightly better, with a loss of 0.95%.

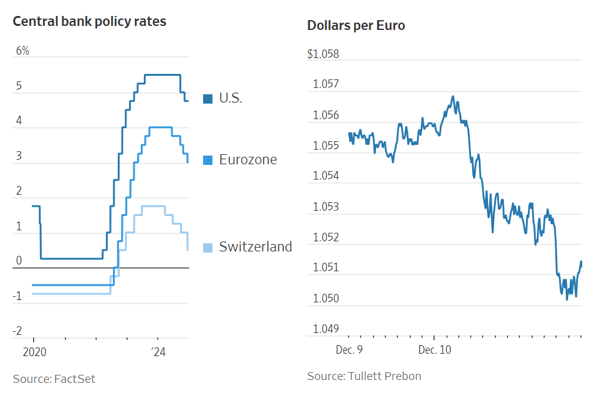

The European Central Bank (ECB) has reduced its key interest rate by 0.25% to 3.00%, marking its third consecutive cut as it seeks to stabilize an economy challenged by debt concerns in France and the looming impact of possible U.S. trade tariffs under President-elect Donald Trump. This move widens the gap between ECB and Federal Reserve borrowing costs, reflecting differing economic pressures across regions. Economic forecasts paint a grim picture for Europe. The ECB projects eurozone growth at just 0.7% in 2024 and 1.1% in 2025, citing heightened risks from political instability in France and Germany, potential U.S. tariffs, and stagnating Chinese demand. The region also faces stagflation pressures, with inflation rising to 2.3% in November while business confidence wanes. Germany’s economy remains stagnant and France faces fiscal challenges, further straining the eurozone's outlook. Investors anticipate further ECB rate cuts, potentially lowering rates to 1.75% by mid-2025, significantly below the Fed’s expected terminal rate. This divergence is placing downward pressure on the euro, which recently dropped below $1.05.

While governments in Germany and France face crises, European firms are grappling with bankruptcies, labor strikes, and leadership shakeups. The lack of standout successes in artificial intelligence (AI) adds to the continent’s woes, particularly when contrasted with the dominance of U.S. firms in market valuation, profitability, and investor confidence. European companies in the STOXX 600 index collectively trade at valuations far below their American counterparts, with shares priced at just 14 times future earnings compared to 23 times for the S&P 500. However, these broad comparisons obscure areas where European firms excel. Europe outshines in industries like pharmaceuticals, where its drugmakers deliver superior returns on capital compared to their American peers. European airlines, luxury brands, and smaller listed firms also outperform their U.S. counterparts in profitability and efficiency. Additionally, a strengthening dollar could boost European exporters, further enhancing their competitive edge. Despite current struggles, Europe’s corporate strengths and low market expectations offer opportunities for recovery. A reversion to historical valuation averages or shifts in global economic dynamics could position European firms for resurgence.

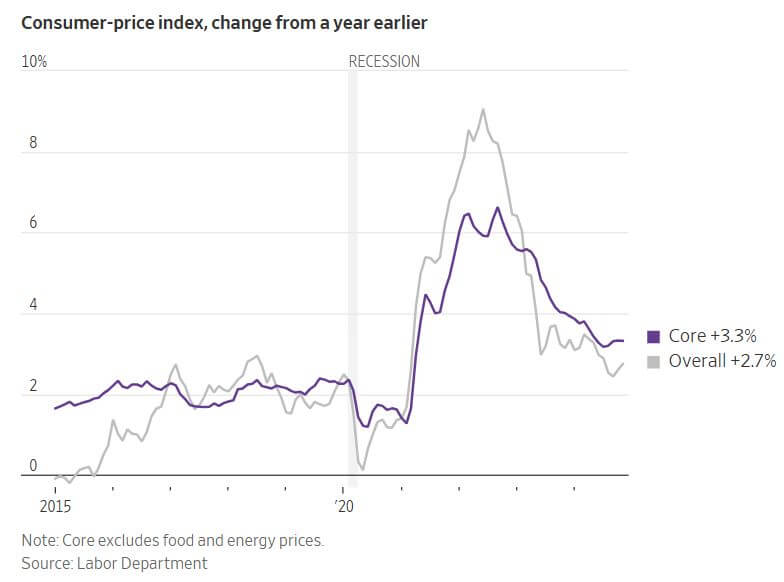

Inflation edged up in November, with the Consumer Price Index (CPI) rising 2.7% year-over-year, slightly above October’s 2.6%. Core inflation, which excludes food and energy, increased by 3.3% over the same period. Monthly CPI growth was 0.3%, the highest since April, driven by higher costs in food, vehicles and medical care. However, housing cost increases moderated, providing some relief. Economists voiced concern about persistent inflation in the services sector and a rebound in core goods prices, particularly vehicles. Economist Sarah House of Wells Fargo noted that the most easily addressable inflationary pressures have been managed, but reducing inflation further will require weakening consumer demand, making progress increasingly difficult. Despite inflationary pressures, U.S. consumer spending remained steady in October, buoyed by strong employment and growing optimism post-election. Business confidence also improved, with indicators like the NFIB small-business optimism index reaching its highest level since mid-2021. The Fed, which has already cut interest rates by 0.75% since September, faces challenges in balancing inflation control with economic growth. The labor market showed resilience in November, with robust job gains, stable unemployment, and steady wage growth at 4% year-over-year. Concerns about future inflation are tied to potential policy changes under the Trump administration, including tax cuts, tariffs, and immigration restrictions, which could stoke inflation further. While mainstream households are regaining confidence and reverting to pre-pandemic spending habits, budget-conscious households continue to feel pressure from prolonged inflation and higher interest rates, underscoring the uneven recovery. Futures markets show that investors are currently expecting the Fed to cut interest rates by a further 0.25% at its upcoming meeting on December 17-18.