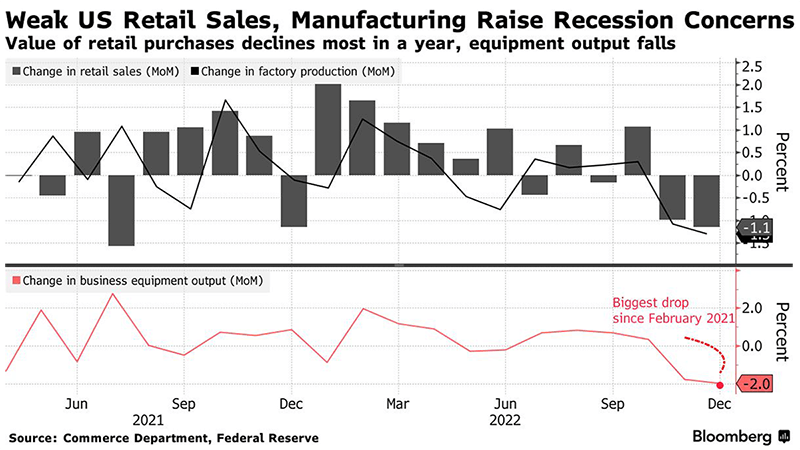

Updated data released last week shows that higher interest rates are continuing to have the expected effect on both inflation and economic activity. On a positive note, the US Producer Price Index (PPI) fell 0.5% in month-on-month terms, significantly more than the surveyed consensus for a 0.1% decline. This was attributed largely to a significant decrease in energy and food prices. Core PPI, which excludes food and energy, rose 0.1% in December compared to the month prior. Compared to a year ago, PPI rose by 6.2% in December, a slowdown from November’s 7.3% rise. Core PPI rose 4.6% in December compared to a year ago, also a slowing from November. However, continued progress on the inflation front came at the cost of slowing economic activity. December US retail sales fell by 1.1% compared to the month prior, marking the second consecutive month of declining consumer spending. That suggests that even despite the holiday shopping season, American consumers are reaching the limits of their spending power. Manufacturing activity also decreased, with a 2% slump in the output of business equipment. That is the second consecutive month of declining business investment. This all suggests that the US Federal Reserve is increasingly likely to raise interest rates by a smaller margin at its next meeting on February 1st.

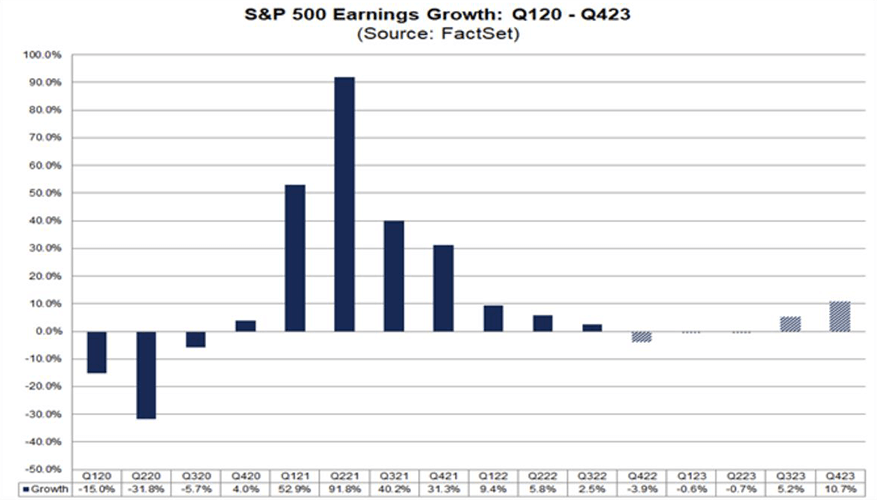

With the fourth quarter earnings season in full swing, FactSet reports that year-over-year earnings growth for the S&P 500 is expected to turn negative. Currently, aggregate earnings for the S&P 500 are forecasted to fall by 3.9% compared to a year ago. Earnings forecasts for 2023 also fell steadily through the second half of the year. While robust earnings growth was previously forecasted for Q1 and Q2 of 2023, today earnings are expected to contract through the first half of the year. Currently earnings are expected to decline by 0.6% in Q1, followed by another contraction of 0.7% in Q2. 10 out of the 11 sectors in the S&P 500 have had earnings estimates revised downward in recent months, with consumer discretionary, communication services, and materials seeing the largest downgrades. This is important, as market price reactions to CPI prints and FOMC meetings have decreased recently, while price movements following earnings beats and misses have risen in magnitude. However, after three consecutive quarters of expected decline, earnings are forecasted to return to growth in the second half of 2023. Third quarter 2023 is forecasted to see earnings growth of 5.2% followed by strong growth of 10.7% in the fourth quarter.

Concerns over the increasing probability of a recession weighed on stocks mid-week. US Treasuries continued their rally through the middle of last week as well. The 10-Year US Treasury note ended last year with a yield of 3.826%. 10-Year yields approached a low near 3.3% mid-week but rose to end the week at 3.483%. Several Fed officials gave relatively dovish comments on Friday, with Fed Governor Christopher Waller noting that monetary policy was close to being sufficiently restrictive and that he was in favor of moderating the pace of interest rate increases. Philadelphia Fed President Patrick Harker also came out in favor of smaller interest rate increases moving forward. However, Fed Vice Chair Lael Brainard reiterated her view that even if the Fed reaches a peak terminal rate soon, interest rate cuts were not soon to follow as inflation remains above the Fed’s target. Equities rallied following the Fed comments on Friday and recouped some of their earlier losses. Despite the late rally, the Dow Jones Industrial Average and S&P 500 still ended down for the week for the first time this year. The Dow fell 2.7% for the week while the S&P 500 fell 0.7%. Despite the higher bond yields to end the week, the Nasdaq Composite managed to post its third week of gains following the announcement of cost-cutting layoffs at several major technology companies.